(Click here for Blog Archive)

(Click here for Blog Index)

(Presentations in this blog were created using the InsMark® Illustration System)

|

Editor’s Note: In Blog #174 Bob introduced you to InsMark’s Dual Security Plan in which owners of a Limited Liability Company, Limited Liability Partnership, or Partnership can fund their buy-sell agreement with life insurance owned by the Company or Partnership. The tax-neutral distribution of property by such entities at retirement provides for a tax-free transfer of the policies to each insured at retirement. This transfer has no tax consequences to the business or insured participant, and each insured can then access income-tax-free cash flow from the life insurance using guaranteed secured loans. No taxes ever — provided the insurance policy is not surrendered, lapsed, sold, or is subject to withdrawals above cost basis. In Blog #201, you will learn how this dynamic concept works for buy-sell agreements between principal owners of C or S corporations. |

Welcome to a new InsMark variation for owners of C or S corporations who can take advantage of the features noted above when positioning their buy-sell arrangement funded with life insurance inside a Limited Liability Company (LLC).

This strategy is a fascinating concept for corporate clients. At first, it may look “too good to be true,” but it applies to all C and S corporations with more than one principal owner. Many traditional buy-sell arrangements will convert to this dynamic convergence of tax law and life insurance. The tax authority does not come from private rulings or tax court decisions or interpretations that say “this” and others that say “that” — and “maybe we can force a new concept to fit.” Not even close — the authority lies in black-letter-law, Internal Revenue Code sections. (See below for the tax citations.)

Tax Analysis

When the policy ownership transfers to the insured at retirement, what are the tax consequences to the LLC? What is the justification for its income-tax-free transfer to members?

The Internal Revenue Code sections governing partnership distributions are different from the ones governing corporations. When a C corporation, for example, distributes a life insurance policy to an employee-owner, the corporation recognizes gain based on its fair market value (which is generally approximated by the policy cash value without regard to any surrender charges). The executive receiving the policy also pays income tax on the fair market value.

With an LLC that has elected partnership taxation (as most do) transfers the policy, the general rule is one of deferral when the distribution involves a K-1 tax form. The LLC recognizes no taxable gain in the transaction, and the Member receiving the policy also has no taxable gain — IRC Secs. 731(a) and 731(b).

In other words, although the LLC’s basis in the policy transfers to the Member, there are no current tax consequences to either party. There are no income taxes ever — provided the insurance policy is not surrendered, lapsed, sold, or is subject to withdrawals above cost basis.

Modern life insurance policies can remain in force until age 120 or the prior death of the insured, and there is no income tax due on the death proceeds of life insurance. The foundation for this particular treatment is IRC Sec. 101(a)(1). This statute provides that the proceeds of life insurance maturing as a death claim are exempt from federal income tax. This exemption applies to the full death benefit, including any cash value component, whether loans exist or not.

Click here for a superb white paper by the Cleveland law firm, Cavitch, Familo & Durkin Co., L.P.A., on the subject of what they refer to as a Life Insurance Limited Liability Company (LILLC) used for funding a Buy-Sell.

Here is their introduction to the white paper:

“This article discusses the benefits, design and application of a specially designed Limited Liability Company to own life insurance that is primarily used to fund Buy Sell agreements between business owners. This is a planning technique developed by the attorneys at Cavitch Familo & Durkin Co., L.P.A. We recognized that there are many benefits to separating life insurance ownership from clients’ operating business. The Life Insurance Limited Liability Company (LILLC) is a separate entity that operates independently from the underlying business and is specifically designed to own insurance contracts on the lives of the business owners. The owners who are the parties to the Buy Sell agreement are also the Members of the LILLC.”

Copyright © 2020, Cavitch Familo & Durkin, Co., L.P.A.

Phone: 216-621-7860; Fax: 216-621-3415

The avoidance of income tax is the secret sauce to the long-term effectiveness of the Dual Security Buy-Sell Plan – based on the following steps:

- The LLC is the purchaser of each life insurance policy. It owns all policy cash values.

- The LLC is initially the beneficiary of each policy’s death benefits. The proceeds finance a buy-sell agreement — either a stock redemption using the LLCs death benefits or a cross-purchase financed by the distribution of the death proceeds to the surviving Member. This distribution is also income tax-free under IRC Sec. 731(a).

With some plans, the death benefit also includes an amount to reimburse the LLC for the insured Member’s lost expertise. The InsMark Illustration System contains a Key Executive Calculator on the Executive Benefits tab for help with establishing the rationale for this amount.

- The life insurance policies are maximum-funded to the extent provided by law.

- Ownership of each policy transfers to the insured Member via a tax-free K-1 distribution at retirement (or a different date or event if agreeable to all parties to the transaction).

- Premiums are typically not scheduled after retirement.

- Each Member uses secured, non-callable, policy loans in post-retirement years to produce tax-free retirement cash flow.

- Each Member keeps the policy in force until death with family members or a trust as the beneficiary.

- Premiums are typically not scheduled after retirement.

- Each Member uses secured, non-callable, policy loans in post-retirement years to produce tax-free retirement cash flow.

- Each Member keeps the policy in force until death with family members or a trust as the beneficiary.

There are several ways to fund the premiums for a Dual Security Buy-Sell Plan:

- Funding Strategy #1: Funds already present in the LLC.

- Funding Strategy #2: The Members make capital contributions to the LLC.

- Funding Strategy #3: The Members’ underlying operating business makes capital contributions directly to the LLC and defines them as follows:

C corporation: Capital contributions are a taxable bonus to the Member1;

S corporation: Capital contributions are an allocation of profits to the Members.

1 This is the funding strategy for Blog #201. Click here to review details of the bonuses.

- Funding Strategy #4: The Members use loan-regime split dollar.

- Funding Strategy #5: The LLC arranges for bank-funded, premium financing with Roger and Tom guaranteeing the bank loan and providing any additional collateral required by the bank.

Note: Blog #202, scheduled for June 2020, will feature the Members and their LLC using this premium financing strategy.

- Funding Strategy #6: The Members combine bank-funded, premium financing with loan-regime split-dollar arrangements.

Illustration software published by InsMark, Inc., can demonstrate each of the funding strategies listed above.

Case Study

Roger Brady and Tom Carpenter, both age 45, are 50/50 shareholders in Battle Lake Ford-Lincoln, Inc. (BLFL), a successful automobile dealership in a large city in Florida. BLFL is a C corporation, and Roger and Tom have been reviewing their current buy-sell arrangement completed a few years ago. They have decided to update it using a Dual Security Buy-Sell Plan that is more appropriate due to its double-barreled tax benefits.

They have formed Brady and Carpenter, LLC, to finance the buy-sell transactions of their shares of BLFL. The Members’ underlying operating business makes capital contributions directly to the LLC in the amount of $200,000 for 20 years. Roger and Tom each report $100,000 of annual ordinary income.

Click here for a Flow Chart of the transaction.

Below are the details of each life insurance policy:

- Male, age 45.

- Policy type: Indexed Universal Life illustrated at 6.50%.

- Face amount of each policy: $3,500,000.

(Increasing for 20 years, level after that.)

- Premium: $100,000 for twenty years.

Pre-Retirement Years

Allocation of each $3,500,000 increasing death benefit:

- $3,000,000, including all of the increasing death benefit, is payable to the LLC for 20 years to fund the buy-sell agreement (reflecting growth of the C corporation for each participant).

- $500,000 of level death benefit for 20 years is dedicated to Key Member indemnification payable to the LLC.

Retirement Starting at Age 65

- Policy death benefits are paid to each Member’s personal beneficiaries.

- Each Member owns all the cash values of the policy.

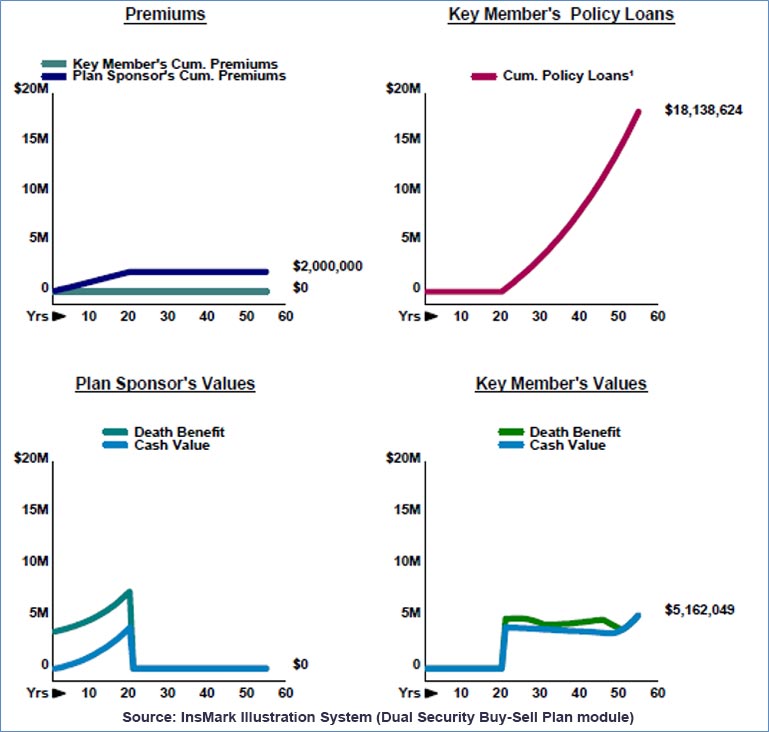

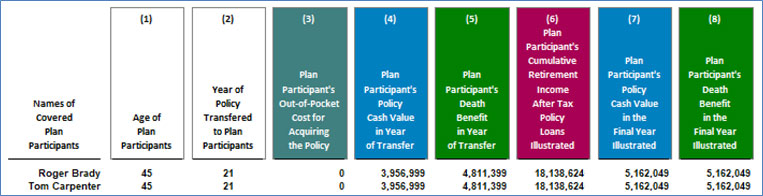

- Each Member receives all tax-free cash flow from the policy using secured, non-callable loans. (Annual cash flow from age 65 to 100 is illustrated at $300,000 and is indexed with a 3.00% cost-of-living assumption, providing total after-tax cash flow of $18,138,624 for each Member.)

Below is a graphic of Roger Brady’s and Tom Carpenter’s results from the Dual Security Buy-Sell Plan sponsored by Brady and Carpenter, LLC:

| Image 1 |

| Dual Security Buy-Sell Plan |

| Plan Sponsor: Brady and Carpenter, LLC |

| Both Roger and Tom are the Same Age; |

| Results Below Apply to Each of Them. |

Below is a Summary of their combined benefits:

Source: InsMark Illustration System (Dual Security Buy-Sell Plans Composite module).

Click here to view the entire Composite of Roger’s and Tom’s illustrations.

The Dual Security Buy-Sell Plan illustration module is available on the Executive Benefits tab in the InsMark Illustration System. Also included in the same location is a module for Composite illustrations for multiple lives. Sample Illustrations of this arrangement are also available in the InsMark Illustration System.

Conclusion

Most of you have access to C and S corporations with multiple owners who will jump at the chance to take advantage of this buy-sell strategy and its powerful, after tax, retirement cash flow (over $18,000,000 each in Roger and Tom’s case.)

Your Comments

What are your thoughts and conclusions after reviewing this material? Please add your comments to this Blog. Your email address will not be published.

Licensing InsMark Systems

To license the InsMark Illustration System or Cloud-Based Documents On A Disk, visit us online or contact Julie Nayeri at julien@insmark.com or 888-InsMark (467-6275). If you are currently licensed for DOD, go to www.insmark.com and select “My InsMark” from the home page for access to the full version of DOD.

Please direct Institutional inquiries to David Grant, Senior Vice President – Sales, at dag@insmark.com or (925) 543-0513.

Complimentary System

For those not licensed for the InsMark Illustration System who would like to review the case-specific, digital workbook files used for this Blog #201, we will be pleased to provide you with a complimentary 30-day installation of the System. Contact Julie Nayeri at julien@insmark.com or 888-InsMark (467-6275) for details.

Specimen Documents

InsMark’s Cloud-Based Documents On A Disk™ (“DOD”) has specimen implementation documents for the Dual Security Buy-Sell Plan in both the Buy-Sell Agreements section and Business Owner Benefit Plans section (see the Limited Liability Company documents in each section). These specimen documents are for licensees to provide to a client’s attorney.

InsMark’s Cloud-Based Documents On A Disk™ (“DOD”) has specimen implementation documents for the Dual Security Buy-Sell Plan in both the Buy-Sell Agreements section and Business Owner Benefit Plans section (see the Limited Liability Company documents in each section). These specimen documents are for licensees to provide to a client’s attorney.

If you are not licensed for InsMark’s Cloud-Based Documents On A Disk™, but would like to learn more about it, click here.

Creating Similar Presentations

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

Workbook files for Blog #201:

|

Before downloading and reviewing any files, be certain you have installed the most current updates to your InsMark System(s). Do this using Live Update available under Help on the main menu bar of the System or this icon on the main menu bar:

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark Systems. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

If you download the Digital Workbook File for Blog #201, click here for a Guide to its content. It will be invaluable to you as you design similar illustrations.

InsMark’s Referral Resources

(Put our Illustration Experts to Work for Your Practice)

We created Referral Resources to deliver a “do-it-for-me” illustration service in a way that makes sense for your practice. You can utilize your choice of insurance company, there is no commission split, and you don’t have to change any current relationships. They are very familiar with running InsMark software.

Please mention my name when you talk to a Referral Resource as they have promised to take special care of my readers. My only request is this: if a Referral Resource helps you get the sale, place at least that case through them; otherwise, you will be taking unfair advantage of their generous offer to InsMark licensees.

Save time and get results with any InsMark illustration. Contact:

- Ben Nevejans, President of LifePro Financial Services in San Diego, CA.

Testimonials

“InsMark has created without question the best suite of software for our industry that has ever existed. I personally have been using their software for almost 30 years, and it changed my career. This unique and user friendly software will add many thousands to your income for as long as you’re in business. InsMark makes me look good, and it will you as well.”

Simon Singer, CFP®, CAP®, RFC®, Past President International Forum, InsMark Platinum Power Producer®, Encino, CA

“The InsMark software is indispensable to my entire planning process because it enables me to show my clients that inaction has a price tag. I can’t afford to go without it!”

David McKnight, Author of The Power of Zero, InsMark Gold Power Producer®, Grafton, WI

“InsMark’s referral resource, Brian Manderscheid from LifePro, has been a gem to work with! He helps us use InsMark with every one of our cases. The genius factor is InsMark’s commitment to “Compared to What.”

Glenn Main, InsMark Platinum Power Producer®, McMurray, PA

“The reason I use InsMark products is because they are so good at explaining financial concepts to all three parties: 1) the producer trying to explain the idea; 2) the computer technician trying to illustrate it; 3) the customer trying to understand it.”

Rich Linsday, CLU, AEP, ChFC, InsMark Power Producer®, Top of the Table, International Forum, Pasadena, CA

“I really thought I knew all the sales techniques that affect my business, but I do now, thanks to InsMark.”

Sam Keck, MBA, CLU, CFP, LUTCF, InsMark Platinum Power Producer®, Financial Planner, Denver, CO

“InsMark is the Picasso of the financial services world — their marketing savvy never fails to amaze me.”

Doug Peete, Past President, Top of the Table, and InsMark Power Producer, Overland Park, KS

“InsMark” and “Wealthy and Wise” are registered trademarks of InsMark, Inc.

“Documents On A Disk” is a trademark of InsMark, Inc.

Important Note #1: The hypothetical values associated with this Blog assume the nonguaranteed values shown continue in all years. This is not likely, and actual results may be more or less favorable. Life insurance illustrations are not valid unless accompanied by a basic illustration from the issuing life insurance company.

Important Note #2: The information in this Blog is for educational purposes only. In all cases, the approval of a client’s legal and tax advisers must be secured regarding the implementation or modification of any planning technique as well as the applicability and consequences of new cases, rulings, or legislation upon existing or impending plans.

Important Note #3: Many of you are rightly concerned about the potential tax bomb in life insurance that can accidentally be triggered by a careless policyowner when policy loans are present and net cash values are so low that the income tax on the gain on surrender (calculated using gross cash values less basis) is more – often significantly more – than the net cash surrender value.

This lurking tax bomb can be present in all forms of whole life and universal life where policy loans of any type are utilized. It can be avoided, and you, the producer, are key to making sure your clients are aware of how to sidestep it.

A tax bomb can be avoided if the policy is neither surrendered nor allowed to lapse, since the policy death benefit wipes away the income tax liability. The foundation of this special treatment is IRC Section 101. This statute provides that the proceeds of life insurance maturing as a death claim are exempt from federal income tax. This applies to the full death benefit, including any cash value component whether loans exist or not.

Note: It is best if you design the policy with no premiums scheduled after retirement if loans are anticipated in retirement years. This may require higher premiums during pre-retirement years, but a policy with no premiums scheduled is much more tolerable at advanced ages than one with continuous premiums.

Can your clients remember these facts years into the future? If they are incapacitated, will family members understand the issues? It is probably best to file a short note with the policy – something like this (although your compliance officer will likely have preferred language):

If/when you take policy loans on this policy, be sure to talk to your financial adviser before surrendering or lapsing the policy in order to anticipate unexpected tax consequences that may otherwise be avoided.

Does this note make it harder or easier to deliver the policy? It’s harder if you haven’t discussed it with your client; easier if you have. And that’s the point – you should discuss it.

Some life insurance companies have concierge units that monitor loan status at the point of lapse or surrender, and you would be well-advised to select an insurance company with this capacity. To be effective regarding the tax bomb, such carriers need to be proactive in their client relationships, not merely reactive to client inquiries. I hope that ultimately the policyholder service division of all life insurance companies will bring this potential liability to the attention of those surrendering or lapsing policies, particularly those policies with 50% or more of the gross cash value subject to outstanding loans.

![]()

More Recent Blogs:

Blog #200: InsMark’s Prudent Care™ Analysis (Part 2)

Blog #199: InsMark’s Prudent Care™ Analysis (Part 1)

Blog #198 How Far Will $1,000,000 Go (Part 2) Joe and Annie Jordan’s Comprehensive Retirement Plan

Blog #197: How Far Does $1,000,000 Go (Part 1)

| 3 Reasons Why It’s Profitable For You To Share These |

| Blog Posts With Your Business Associates and |

| Professional Study Groups (i.e. “LinkedIn”) |

Robert B. Ritter, Jr. Blog Archive