(Presentations were created using the InsMark Business Valuator and Wealthy and Wise®.)

This Blog is written in coordination with our webinar featuring the InsMark Business Valuator (powered by BizEquity), the best lead generation system ever invented for successful business prospecting. Whether you are already active in the business market or would like to break into it, we hope you haven’t missed this webinar. If you did, we recorded it and you can click here to view it on the InsMark YouTube Channel.

The webinar features Don Prehn, marketing consultant and past President of InsMark, as he explains why this Cloud-based, business valuation service can completely change the way you interact with business owners (and enhance virtually everything you can do for them).

For those who become involved with this new concept, InsMark will share Case Studies in the next several Blogs to help you get up to speed on this exciting new platform. This Blog #41 begins the process.

Case Study #1

George and Marie Grove are age 65 and 60 and run a successful business. They are asking this question:

“If we sell our business for what we think it’s worth,

can we have the retirement cash flow we want

and still have a comfortable level of ongoing net worth?”

| The Groves have the following assets: | |

|---|---|

| $ 700,000 | Taxable Accounts |

| $ 900,000 | Tax Exempt Accounts |

| $ 750,000 | George’s IRA |

| $ 900,000 | Marie’s IRA |

| $ 4,762,500 | Equity Account (incl. the after tax proceeds of $3,762,500 from a current sale of their closely-held business valued at $5,000,000) |

| $ 1,200,000 | Illiquid Assets (personal property and home scheduled for downsizing in five years) |

| $ 9,212,500 | Total |

|

Query: If you are involved in retirement and/or estate planning with clients who own their own business, can you do it accurately without knowing a realistic value of the business? You really can’t, particularly by a seat-of-the pants guess by their advisers, but reliable valuations typically cost $8,000 to $15,000. Good for one year of continuous analysis, each BizEquity valuation costs a client $350 (and as low as $150 each if you purchase 20 valuations in a package). The results are based on a national data base of comparables of similar businesses in similar geographic locations.

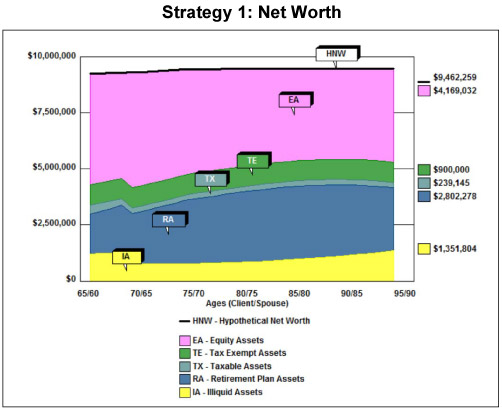

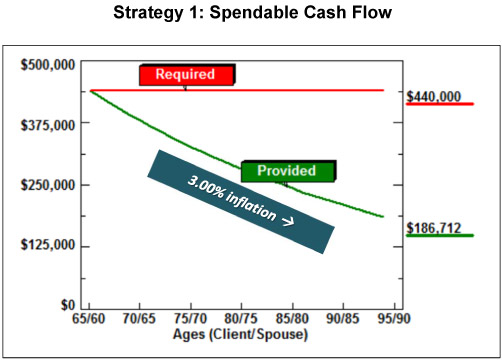

We will use InsMark’s Wealthy and Wise to find out how much spendable cash flow can be produced for George and Marie from their current assets while retaining close to their current level of net worth.

|

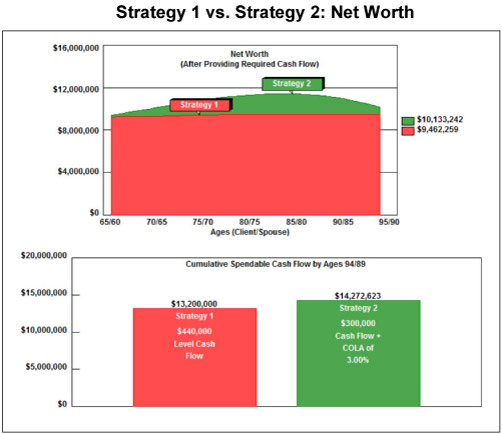

There is, however, a problem. The buying power of $440,000 diminishes rapidly due to inflation.

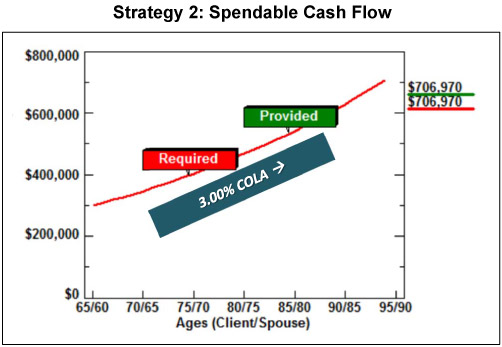

Strategy 2: The cash flow and residual net worth work out better if we schedule $300,000 of cash flow with a cost-of-living-adjustment (“COLA”) in an attempt to deal with inflation. Under this assumption, the after tax cash flow looks like this:

Total cash flow under these assumptions is $14,272,623 which is $1,972,623 more than the $13,200,000 provided in Strategy 1: Spendable Cash Flow.

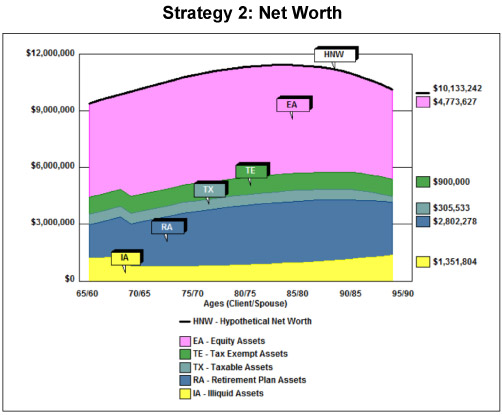

Net worth now looks like this:

Let’s compare the two side-by-side. Strategy 2 produces an attractive net worth solution.

Case Study #2

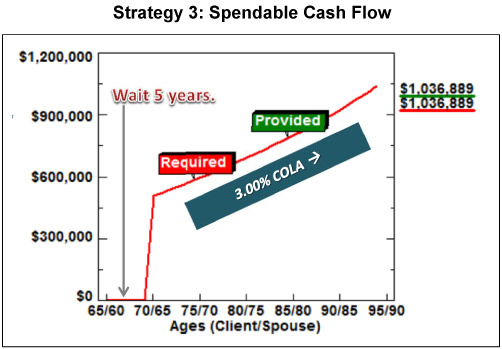

Strategy 3: George asks how the numbers will look in five years. He expects his business to grow by 10% a year. Marie asks if that plan can support the original $440,000 spendable cash flow plus the 3.00% COLA — and it does.

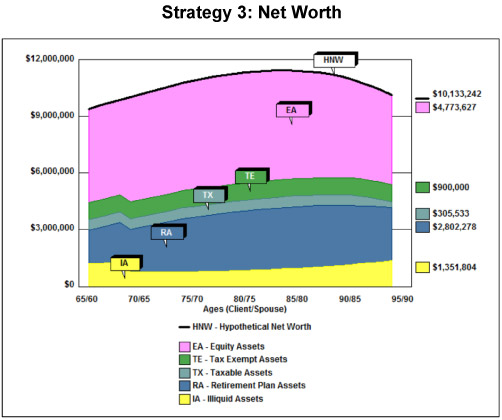

As you can see below, their net worth adjusts accordingly, but ends up in about the same place.

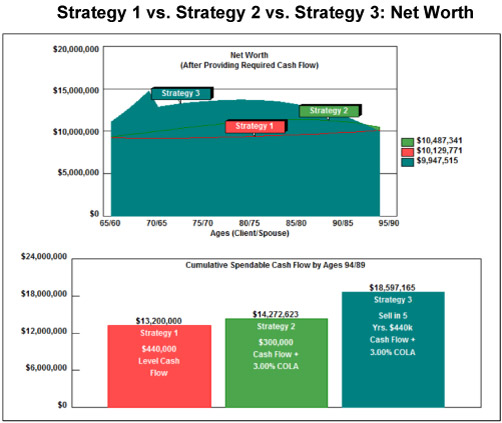

Let’s look at all three Strategies together:

Strategy 3 is impressive. George and Marie’s net worth ends up consistent with their target. Their goal of COLA-adjusted spendable cash flow of $440,000 is also met (producing cumulative cash flow several millions higher than either Strategy 1 or 2.)

Strategic Point: There is no other planning software that can accomplish this analysis other than the combination of BizEquity and Wealthy and Wise.

Now your planning skills come into play. What moves must George and Marie make to ensure these results? I’m certain that several will have occurred to you already. Our solutions will be forthcoming starting with Blog #42 scheduled for release on Thursday, February 27, 2014.

Click here if you would like to review the Wealthy and Wise reports for the three Strategies. The system generates a substantial number of reports because we back up every number we calculate. We never want to leave you flat-footed when a CPA or attorney asks, “Where did this number come from?” For an actual proposal, you will probably want to include a few key reports particular to your case and put the balance in a carefully organized Appendix.

Issues for you to think about:

- George is one of the key executives needed to produce the 10% growth in the value of the business over the next five years.

- George tells us that Tom Hamilton, Executive Vice President and non-shareholder, is also key to the growth of the business.

Over the next few weeks, we’ll begin examining several ways to address these issues. I hope you’ll offer yours by way of Comments to the Blog.

Final Note: The first financial professional who provides access to the InsMark Business Valuator (powered by BizEquity) to a given business owner is the one who wins. There is absolutely nothing for advisers who later offer it to that same business owner. As a result, we are promoting BizEquity to the InsMark user base first to give those most closely associated with us first crack at it; however, we will be offering it widely to others later this year.

For information about BizEquity or licensing information regarding Wealthy and Wise, contact Julie Nayeri at julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President – Sales, at dag@insmark.com or 925-543-0513. (Several of our life insurance company clients are looking at it.)

InsMark’s Digital Workbook Files

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

Digital Workbook Files For This Blog

Download all workbook files for all blogs

|

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark System. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

InsMark’s Referral Resources

(Put our Illustration Experts to Work for Your Practice)

We created Referral Resources to deliver a “do-it-for-me” illustration service in a way that makes sense for your practice. You can utilize your choice of insurance company, there is no commission split, and you don’t have to change any current relationships. They are very familiar with running InsMark software.

Please mention my name when you talk to a Referral Resource as they have promised to take special care of my readers. My only request is this: if a Referral Resource helps you get the sale, place at least that case through them; otherwise, you will be taking unfair advantage of their generous offer to InsMark licensees.

Save time and get results with any InsMark illustration. Contact:

- Ben Nevejans, President of LifePro Financial Services in San Diego, CA.

Testimonials:

“I am writing to give you a ringing endorsement for the Wealthy and Wise System. As you know, I am a LEAP practitioner. The Wealthy and Wise software has helped me supplement my LEAP skills in the over age 60 client base. I have been paid for many cases using Wealthy and Wise as support, the smallest of which was $27,000, the largest was $363,000. With those type of commissions, you would have to be nuts not to buy it.”

Vincent M. D’Addona, CLU, ChFC, MSFS, AEP, InsMark Power Producer, New York, NY

“If you don’t get the client to distinguish cash flow from net worth, you won’t make the case sale. In my experience, Wealthy and Wise is the only system that recognizes this important estate planning component.”

Stephen Rothschild, CLU, ChFC, CRC, RFC, International Forum Member, Saint Louis, MO

![]()

More Recent Blogs:

Blog #40: Leveraged Deferred Compensation

Blog #39: More on the Magic of Indexed Universal Life

Blog #38: Avoiding a $20 Million Mistake

Blog #37: Four Ways to Smite a Termite

Blog #36: The Magic of Indexed Universal Life

| 3 Reasons Why It’s Profitable For You To Share These |

| Blog Posts With Your Business Associates and |

| Professional Study Groups (i.e. “LinkedIn”) |

Robert B. Ritter, Jr. Blog Archive