Blog #221 Testing Financial Tolerance

for Zero Estate Tax with

Loan-Based Private Split-Dollar and Wealthy and Wise

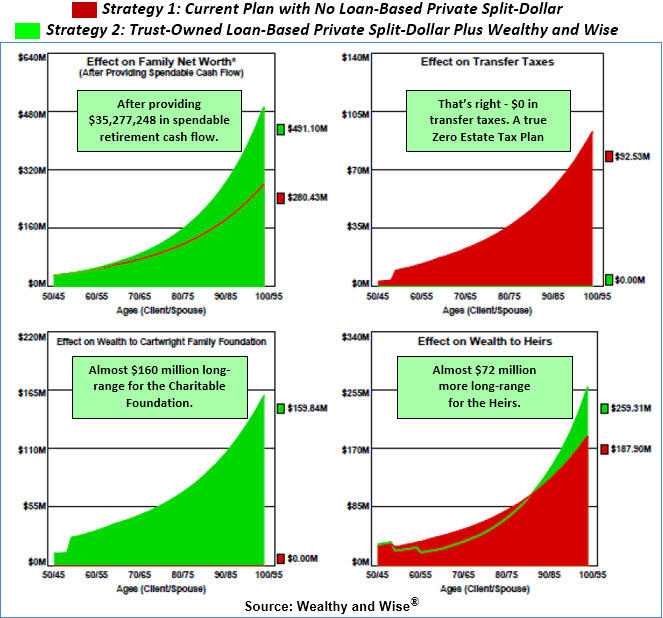

Trust-Owned Loan-Based Private Split-Dollar is an exceptional transaction. Results like those shown above occur when you combine it with InsMark’s Wealthy and Wise.®

Integrating Loan-Based Private Split-Dollar into Wealthy and Wise provides a contextual analysis that reinforces the value of this unique strategy.

It makes little difference which planning strategy you use: split-dollar, private split-dollar, premium financing, GRAT, SCIN, private annuity, or family limited partnership. They all lend themselves to the lens of Wealthy and Wise as an innovative tool for comparative evaluations.

You can read the rest here: Blog #221 . . .

![]()

Blog #220 Testing Financial Tolerance

for Zero Estate Tax™

-493x203.jpg)

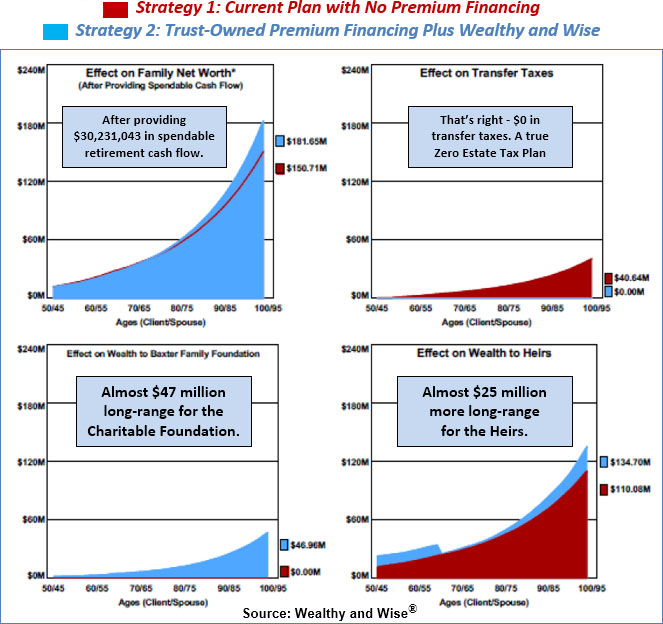

Bank-funded Premium Financing can be an exceptional transaction. You can develop results like those shown below when you combine it with InsMark’s Wealthy and Wise®,

Long-range controlled wealth totals over $181 million. “Control of wealth is the virtual equal of ownership of wealth.”

Dr. John Rutledge, PhD, Chief Investment Strategist, Safanad.

Integrating the Premium Financing into Wealthy and Wise provides a contextual analysis that reinforces the value of premium financing.

It makes little difference which estate planning strategy you use. Premium financing, split-dollar, private split-dollar, GRAT, SCIN, private annuity, and family limited partnership all lend themselves to the lens of Wealthy and Wise as an innovative tool for comparative evaluations.

You can read the rest here: Blog #220 . . .

![]()

Blog #219: Exceptional Split-Dollar™ (Part 1 of 2)

(Including a “Jim Harbaugh” Variation to

Recruit a President for a Tax Exempt University)

In the past few years, there has been substantial publicity about the University of Michigan providing a high-end, split-dollar plan for its head football coach, Jim Harbaugh. So, let’s review a similar arrangement for another significant Tax Exempt University to see how the concept works for attracting Roger DeWitt Thompson, H’94 ’95 ’98. Roger is the University’s top candidate for President.

You can read the rest here: Blog #219 . . .

![]()

Blog #218: Attracting and

Retaining Key Executives

Ask this question of any business owner:

Do you have any executives who are so valuable that you would do almost anything that is financially responsible to keep or hire them?”

You can read the rest here: Blog #218 . . .

![]()

Blog #217: Tax Bombs That Never Exploded

(More on Grantor Trusts)

It looks like U.S. estate planning has escaped the tax bombs Democrats wanted to drop with Joe Biden’s Build Back Better (BBB). So it’s back to rational planning concepts, like the intentionally defective grantor trust (“IDGT”).

If you have clients and prospects with wealth somewhere north of at least $15 million, get them to consider the tremendous advantages of these trusts.

Many of InsMark licensees tell us that our do-it vs. don’t-do-it™ approach is a terrific door-opener-closer. Read Blog #217 to see how we use it with IDGT.

You can read the rest here: Blog #217 . . .

![]()

Blog #216: Cost of Waiting

(Delay is the Deadliest Form of Denial)

You should acquire your life insurance as soon as you determine its usefulness. That’s when your health may be the best it will ever be, and the benefits are more favorable the sooner you act.

Blog #216 proves the efficiency of buying now — regardless of the strategy utilized.

Life insurance is often considered a postponable purchase. This presentation can help you add an element of urgency to the deliberation.

You can read the rest here: Blog #216 . . .

![]()

Blog #215: Three Good Ideas

I recently reviewed some of my earlier Blogs. Three of them involved sales thoughts, not illustrations. They seemed worthwhile repeating, and here are the links:

Tell Me What’s Wrong With It

Identifying Good Prospects; Discarding Bad Ones

It’s Awkward Trying to Sell My Friends

You can read more about them here: Blog #215 . . .

![]()

Blog #214:

Roth Conversion Magic

Blog #214: Roth Conversion Magic, I used the extraordinary mathematics of Wealthy and Wise® to analyze a challenging tax issue and proved that the income tax on a Roth Conversion can be an excellent investment. The analytical advantage of using a “Compared to What?” evaluation makes Wealthy and Wise® unusually effective.

The source for the $14+ million cumulative after-tax cash flow ($250,000 annually, indexed for inflation) is the clients’ liquid assets with $0 personal out-of-pocket required.

I am unaware of any other software that takes this complex approach to produce an easily understandable assessment for you, your clients, and their advisers.

You can read the rest here: Blog #214 . . .

![]()

Blog #213: Missed our May 2021 Virtual Symposium?

Did you miss our May 2021 Virtual Symposium? Don’t worry. You can register now for FREE to access the meeting recordings, PowerPoints, and the many resources from our Exhibit Hall Booths.

If you are interested, don’t delay — registration is available only through September 19 when Cvent, our platform sponsor, takes down our site.

You can read the rest here: Blog #213 . . .

![]()

Blog #212: InsMark’s Introduction to the Ultimate Professional Coach

This Blog is a departure from my usual format featuring Case Studies. However, information about the Center for Tax, Strategies & Resources is vital. I want you to know about it to understand how much I believe in this premier organization and its usefulness for many of you.

You can read the rest here: Blog #212 . . .

![]()