(Click here for Blog Archive)

(Click here for Blog Index)

(Presentations in this blog were created using the Leveraged Compensation System)

Background

You met Tony Jamison in Blog #203 – Anybody Want A Free Dog (Part 1 of 2). Tony is Executive Vice President and General Manager of Town and Country Auto Group, Inc., a multi-brand, multi-city, new car dealership based in Austin, TX, operating as an S Corporation. Tony, age 45, continues to be a significant rainmaker for Town and Country; however, the company is a family business, and Tony does not expect to be a shareholder. The company is vitally interested in providing him with irresistible executive benefits to ensure his employment for several years.

In Blog #203, Town and Country rewarded Tony with a benefit called an Executive Bonus Plan that provides him with $260,000 of after-tax retirement cash flow from age 65 to 100. Funded with indexed universal life (IUL), the plan also provides his family with a substantial tax-free death benefit.

We did not want Tony to have any out-of-pocket tax cost on the funding of the plan or require Town and Country to use a gross-up bonus to offset the tax. As a result, in pre-retirement years, we used tax-free participating loans on the IUL policy to offset the tax on a single bonus.

Blog #204 provides an identical, more efficient retirement benefit for Tony. We used a taxable bonus coupled with a variation of loan regime split-dollar that supplies the cash flow for that tax. Like Blog #203, the revised plan also produces $260,000 of annual, after-tax, retirement cash flow for Tony. With the Leveraged Executive Bonus, if Tony dies before retirement, part of the policy death benefit repays the split-dollar loan. At the same time, his family receives tax-free life insurance proceeds of $10 to $14 million.

Town and Country’s overall cost for the Leveraged Executive Bonus is $600,000 compared to the $1,200,000 spent in Blog #203.

Tony was also featured in Blog #136: Taking Care of a Rainmaker where we used InsMark’s Executive Trifecta® to produce a similar $260,000 of tax-free retirement cash flow, identical to the amount available in Blogs #202 or #203. As a valued non-owner key executive, a combined total of $520,000 of annual, tax-free retirement cash flow goes a long way toward convincing Tony that staying with Town and Country is a smart, long-range decision.

Tony was also featured in Blog #136: Taking Care of a Rainmaker where we used InsMark’s Executive Trifecta® to produce a similar $260,000 of tax-free retirement cash flow, identical to the amount available in Blogs #202 or #203. As a valued non-owner key executive, a combined total of $520,000 of annual, tax-free retirement cash flow goes a long way toward convincing Tony that staying with Town and Country is a smart, long-range decision.

Town and Country has selected the Leveraged Executive Bonus as the new benefit plan for Tony. See below for details.

Leveraged Executive Bonus

There are two critical issues when designing a plan including loan regime split-dollar:

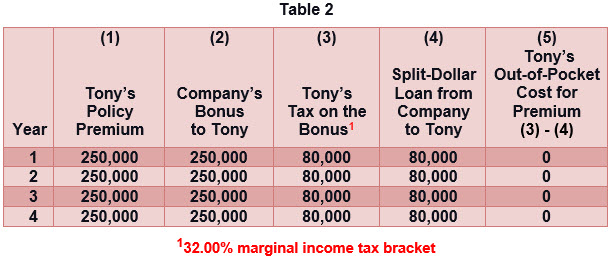

- The length of the premium payment period. Due to the extraordinarily low level of the current, long-term applicable federal rate (AFR), the fewer premiums, the better, because loan interest will lock down with extremely low, long-term AFRs for all 20 years of split-dollar loans. We selected four premiums of $250,000, which produces the same $260,000 of annual tax-free retirement cash flow as Blog #203. Further, this 4-pay approach eliminates classifying the IUL as a modified endowment contract (MEC) thus avoiding its unpleasant taxation.

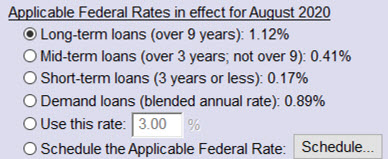

- Which AFR to select? Here are the options for August 2020:

- Ignore demand loans (blended annual rate) as they changes annually, a scenario that is impossible to forecast sensibly.

- The short-term rate of 0.17% is tempting until you realize it has to be recast every three years at the new short-term rate. With the skyrocketing debt of the U.S. government, we will ultimately see steeply-rising AFRs affecting many of the years of split-dollar loans.

- A similar problem exists with mid-term loans. Select this AFR if you want to risk a severe increase every nine years.

- That leaves the long-term loan rate that never requires an increase once made. With four premiums, this AFR is my preferred choice.

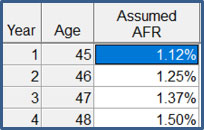

Do you think AFRs will spike over the next four years? On Wednesday, June 10, 2020, Fed Chairman Jerome Powell “committed the Fed to do whatever we can for as long as it takes to support the economy.” Fed officials projected no plans to raise interest rates through 2022. This commitment means the AFRs will likely remain low for several years. I prefer illustrating a small, potential increase in the long-term AFR over the remaining premium-paying years for Tony’s plan, as shown in Table 1.

| Table 1 | |

|

In Table 1, I scheduled a slightly increasing assumption for the long-term AFR over the beginning four years of the split-dollar loans that fund Tony’s plan. So long as the loan interest rate on each loan is equal to the long-term AFR established under IRC Secs. 7872(f)(2)(A) and 1274(d) at the inception of the loan, no further interest is imputed to the executive. |

With a four-pay premium, the long-term AFR freezes on all loans after four years. Too conservative? Maybe. Too liberal? Maybe. The best authorities to make the decision are a client’s legal and tax advisers; however, I stand by my selections for Tony’s plan in Table 1 as reasonable projections. I recommend selecting the long-term AFR coupled with the shortest premium-paying period that avoids a MEC.

I believe the U.S. Treasury Department decided to make loan regime split-dollar as complicated and challenging as possible in line with their dislike of split-dollar ever since Rev. Rul. 55-713 first appeared 65 years ago. But it backfired on them. I believe a correctly constructed loan regime split-dollar is more effective than pre-2000 equity split-dollar. The only variable is the unknown, future AFRs, so select long-term rates using reasonable projections coupled with the fewest number of premiums possible.

Executive’s Plan Costs

Tony may have other out-of-pocket costs based on the selection of loan interest payments. Click here to review how each one works out for Tony.

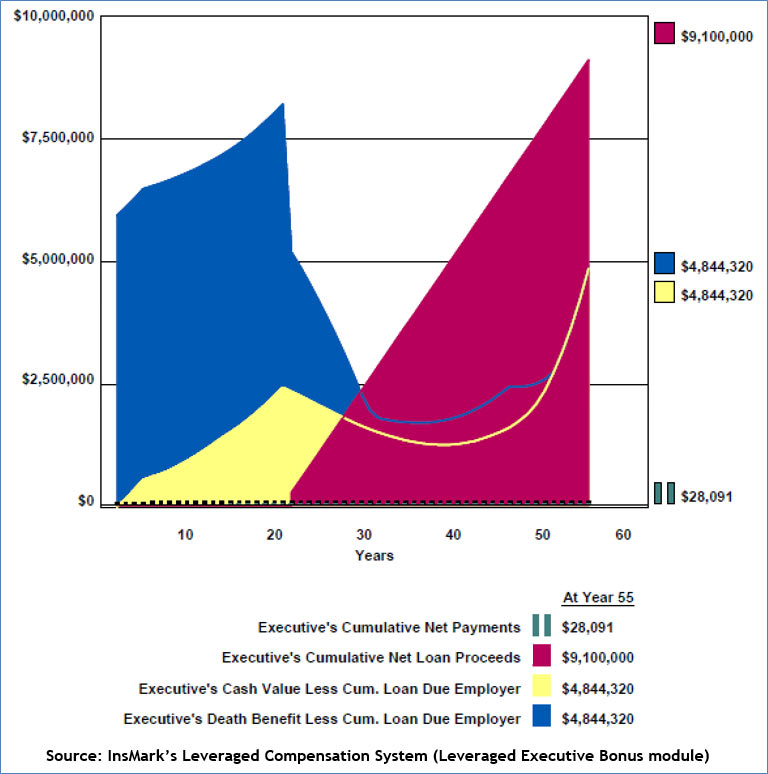

Below is a graphic of Tony’s costs and benefits.

Click here to review the entire presentation.

Range of Uses

The Leveraged Executive Bonus is not appropriate for top executives of publicly-owned companies (thanks to the Sarbanes-Oxley prohibition of loans to such individuals).

It can be used effectively by any executive (owner or otherwise) of a C corporation. It also works well for non-owner key executives of C corporations, S corporations, LLCs, LLPs, and charitable organizations.

Conclusion

The Leveraged Executive Bonus is usually more efficient for all parties than traditional Executive Bonus or Loan Regime Split-Dollar used separately. It is classic executive-owned life insurance (ExOLI) as opposed to corporate-owned life insurance (COLI).

From the insured participant’s perspective, ExOLI beats COLI hands-down due to:

- Direct payment to beneficiaries of the policy’s tax-exempt death benefits;

- Tax-free nature of the retirement benefits; and

- Immediate vesting.

Your Comments

What are your thoughts, conclusions, or questions after reviewing this material? Please add your comments to this Blog. Your email address will not be published.

What’s Next?

In Blog #205: New Wealth Planning, we will announce an advanced version of Wealthy and Wise®, InsMark’s wealth planning system, designed to feature the multiple uses of Grantor Trusts. Emphasis will be on planning methods to circumvent large increases in death taxes.

Licensing InsMark Systems

To reproduce similar “Leveraged Executive Bonus” illustrations, license our Leveraged Compensation System. Visit us online, or contact Julie Nayeri at julien@insmark.com or 888-InsMark (467-6275).

There is a special 50% discount on both the initial and ongoing maintenance fees1 of all our Systems available through September 2020. Use the discount code POWER to take advantage of this special offer.

1The maintenance fee provides free upgrades, enhancements, and technical support.

Institutional inquiries — contact David Grant, Senior Vice President – Sales, at dag@insmark.com or (925) 543-0513.

Specimen Documents

InsMark’s Cloud-Based Documents On A Disk™ (“DOD”) has specimen implementation documents for Leveraged Executive Bonus in the Key Employee Benefit Plans section along with hundreds of other benefit, estate, and charitable planning techniques available for licensees to study or provide to attorneys and CPAs.

InsMark’s Cloud-Based Documents On A Disk™ (“DOD”) has specimen implementation documents for Leveraged Executive Bonus in the Key Employee Benefit Plans section along with hundreds of other benefit, estate, and charitable planning techniques available for licensees to study or provide to attorneys and CPAs.

If you are currently licensed for DOD, click here for access. (Once you log in, click on the DOD icon.)

If you are not licensed for DOD, but would like to learn more about it, click here or you can contact Julie Nayeri at julien@insmark.com or 888-InsMark (467-6275).

Institutional inquiries — contact David Grant, Senior Vice President – Sales, at dag@insmark.com or (925) 543-0513.

Creating Similar Presentations

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files. Also be sure to download the “Guide to Digital Workbook File for Blog #204.pdf” also available below.

If you would like highly qualified, illustration design assistance with no commission split required, contact LifePro Financial, InsMark’s Referral Resource, discussed below.

Digital Workbook Files

For those licensed for the Leveraged Compensation System, click the link below:

|

Before downloading and reviewing any files, be certain you have installed the most current updates to your InsMark System(s). Do this using Live Update available under Help on the main menu bar of the System or this icon on the main menu bar:

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark Systems. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

If you download the Digital Workbook File for Blog #204, click here for a Guide to its content. It will be invaluable to you as you design similar illustrations.

InsMark’s Referral Resources

(Put our Illustration Experts to Work for Your Practice)

We created Referral Resources to deliver a “do-it-for-me” illustration service in a way that makes sense for your practice. You can utilize your choice of insurance company, there is no commission split, and you don’t have to change any current relationships. They are very familiar with running InsMark software.

Please mention my name when you talk to a Referral Resource as they have promised to take special care of my readers. My only request is this: if a Referral Resource helps you get the sale, place at least that case through them; otherwise, you will be taking unfair advantage of their generous offer to InsMark licensees.

Save time and get results with any InsMark illustration. Contact:

- Ben Nevejans, President of LifePro Financial Services in San Diego, CA.

Testimonials

“The InsMark software is indispensable to my entire planning process because it enables me to show my clients that inaction has a price tag. I can’t afford to go without it!”

David McKnight, Author of The Power of Zero, InsMark Gold Power Producer®, Grafton, WI

“The reason I use InsMark products is because they are so good at explaining financial concepts to all three parties: 1) the producer trying to explain the idea; 2) the computer technician trying to illustrate it; 3) the customer trying to understand it.”

Rich Linsday, CLU, AEP, ChFC, InsMark Power Producer®, Top of the Table, International Forum, Pasadena, CA

“InsMark is the Picasso of the financial services world — their marketing savvy never fails to amaze me.”

Doug Peete, Past President, Top of the Table, and InsMark Power Producer, Overland Park, KS

“Bob Ritter is a master of illustrating complex issues in a simple easy-to-use manner that definitely helps you better serve your clients.”

Gary Curry, President and CEO, ORBA Insurance Services, Inc., InsMark Platinum Power Producer®, Gold River, CA

“InsMark”, “Executive Trifecta”, the InsMark Logo are registered trademarks of InsMark, Inc.

“Documents On A Disk” is a trademark of InsMark, Inc.

Copyright © 2020 InsMark, Inc.

All Rights Reserved

Important Note #1: The hypothetical values associated with this Blog assume the nonguaranteed values shown continue in all years. This is not likely, and actual results may be more or less favorable. Life insurance illustrations are not valid unless accompanied by a basic illustration from the issuing life insurance company.

Important Note #2: The information in this Blog is for educational purposes only. In all cases, the approval of a client’s legal and tax advisers must be secured regarding the implementation or modification of any planning technique as well as the applicability and consequences of new cases, rulings, or legislation upon existing or impending plans.

Important Note #3: There is a potential tax bomb in life insurance that can accidentally be triggered by a careless policyowner. This unfortunate development occurs when policy loans are present, and net cash values are so low that the income tax on the gain on surrender can be significantly more than the net cash surrender value.

This lurking tax bomb can be present in all forms of whole life and universal life where policy loans of any type are utilized. Be sure your clients are aware of how to sidestep it.

The tax bomb can be avoided if the policy is neither surrendered nor allowed to lapse since the policy death benefit wipes away the income tax liability. The foundation of this particular tax treatment involves IRC Section 101. This statute provides that the proceeds of life insurance maturing as a death claim are exempt from federal income tax. This exemption applies to the full death benefit, including any cash value component, whether or not loans exist.

Note: It is best to design the policy with no premiums scheduled after retirement if loans may occur in retirement years. This design may require higher premiums during pre-retirement years, but a policy with no premiums scheduled is much more tolerable at advanced ages than one with continuous premiums.

Can your clients remember these facts years into the future? If they are incapacitated, will family members understand the issues? It is probably best to file a short note with the policy – something like this (although your compliance officer will likely have preferred language):

If/when you take policy loans on this policy, be sure to talk to your financial adviser before surrendering or lapsing the policy in order to anticipate unexpected tax consequences that may otherwise be avoided.

Does this note make it harder or easier to deliver the policy? It’s harder if you haven’t discussed it with your client; easier if you have. And that’s the point – you should discuss it.

Some life insurance companies have concierge units that monitor loan status at the point of lapse or surrender. You would be well-advised to select an insurance company with this capacity as carriers need to be proactive in their client relationships, not merely reactive to client inquiries. I hope that the policyholder service division of all life insurance companies will ultimately bring this potential liability to those surrendering or lapsing policies, particularly those with 50% or more of the gross cash value subject to outstanding loans.