(Click here for Blog Archive)

(Click here for Blog Index)

(Presentations in this Blog were created using InsMark’s Wealthy and Wise® and the InsMark® Illustration System.)

In Blog #175 (Part 1 of 2), we examined a Roth conversion for Robert and Ann Baxter, both age 60 and in a 33% income tax bracket. The purpose of the analysis was to gauge whether the income tax cost of the conversion could be considered a good investment. As it turned out, the $1,915,723 in increased long-range net worth reflects a pre-tax, equivalent, rate of return of 9.10% on the conversion’s income tax costs of $256,292. The fact that their heirs could inherit a Roth IRA instead of an IRA adds considerable weight to the overall effect.

We funded the Baxter’s $600,000 Roth IRA over ten years to make sure their income tax bracket of 33% doesn’t increase as it would if the conversion occurred all in one year.

If clients are currently in the highest bracket (37% federal + state), you may want to assume an increase beyond that won’t occur, but how sure are you? More important, how sure are your clients? Given our politicians’ rabid search for more revenue coupled with the current real debt (not $20 trillion, but close to $120 trillion and climbing if you count unfunded liabilities like Social Security, Medicare, etc.), what are the chances for increased income taxes in the future? Very likely, I think. Click here for a history of U.S. income tax rates. As recently as 1980, the federal rate alone was 70%.

Case Study

So, let’s analyze income tax for wealthier clients. Kerry and Amanda O’Neill are both age 60 and in the top 37% federal tax bracket plus a 12.3% state income bracket. Further, the 12.3% is no longer deductible since state and local property, income, and sales taxes already take the O’Neills past the $10,000 limit on how much they can deduct. The 2017 Tax Reform legislation has landed them in a marginal income tax bracket of 49.3% (combined federal and state).

We will analyze their wealth plan from that perspective and then do it again assuming an increase in their combined tax bracket to 75% (federal and state) at retirement in ten years.

The O’Neills own a successful real estate agency currently valued at $5,000,000 which they expect to sell within ten years (prior to retirement). Including the agency, their net worth is $9,850,000 consisting of $2,000,000 in an IRA, $400,000 in taxable accounts, $800,000 in tax exempt accounts, $1,200,000 in equities plus $1,000,000 in home value, and $250,000 in personal property. They have an $800,000 mortgage on their home and no other debt.

Their retirement goal is to have $400,000 of annual, after tax, cash flow indexed at 3.00% starting at age 70 while maintaining at least a level amount of net worth throughout their retirement. Also scheduled is $25,000 in annual travel expenses beginning at age 70 (with the same indexing).

Click here to review the details of their current net worth.

Kerry and Amanda are considering the conversion of their $2,000,000 in retirement plan funds to a Roth, but the resulting $966,000 of income tax is a sticking point – even if they space it over several years.

“We just don’t want any voluntary tax increases – we pay enough as it is,” says Amanda.

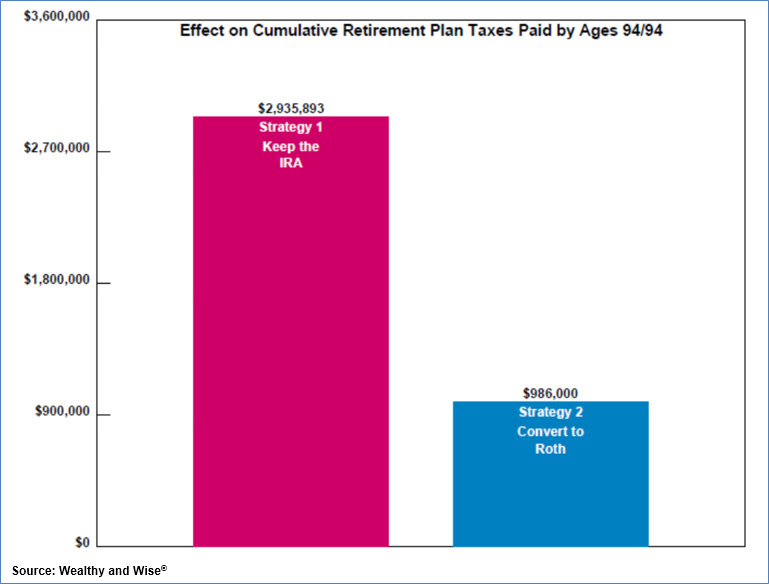

“Let me show why income tax can represent a good investment,” responds their adviser, “look at the difference in your taxation in this graphic – even if you convert your $2,000,000 IRA all in one year.”

| Image 1 |

| 49.3% Tax Bracket in All Years |

| Strategy 1: Keep the IRA |

| vs. |

| Strategy 2: Convert to a Roth |

Retaining the IRA costs almost three times as much in income tax compared to the income tax on the Roth conversion.

Click here to see the numerical report.

“I see that,” says Kerry, “but the Roth conversion tax is due all at once.”

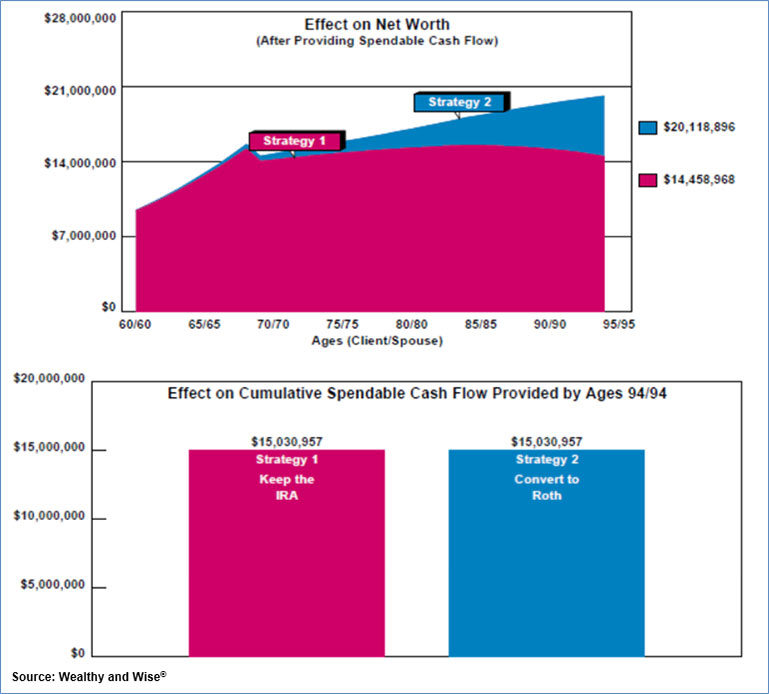

“Wait until you see the other half of the map,” responds the adviser, “the Roth not only avoids almost $3,000,000 in IRA taxes, it adds over $5,000,000 to your long-range net worth while also meeting your retirement cash flow goal.”

“But we have an immediate, out-of-pocket cost of $966,000 in income tax to get the Roth,” responds Amanda.

“It’s not out-of-pocket the way I designed the plan,” responds their adviser. “The tax is funded using a withdrawal from your current assets. The Roth is so powerful it more than recovers the cost of that withdrawal.”

| Image 2 |

| 49.3% Tax Bracket in All Years |

| Strategy 1: Keep the IRA |

| vs. |

| Strategy 2: Convert to a Roth |

While absorbing the $966,000 in conversion tax, the Roth produces a gain of $5,659,928 in long-range net worth. When you don’t integrate a Roth conversion within an overall wealth analysis like Wealthy and Wise, this result is typically lost. If you don’t show this effect, 1) you will make fewer Roth conversions and 2) you had better hope your competition doesn’t show it either.

Note: In the O’Neills’ marginal tax bracket of 49.3%, they would have to earn an annual, pre-tax, compound rate of return of 10.219% to turn $966,000 into $5,659,928 over 35 years. (You can view proof of this after Image 4.)

As you can see in the two bar graphs at the bottom of Image 2, the net worth of either strategy also produces Kerry and Amanda’s desired, annual, after tax, retirement cash flow of $400,000 indexed at 3.00% starting at age 70. This totals $15,030,957 through their age 95 – five years past their joint life expectancy of age 90.

Income Tax Increase

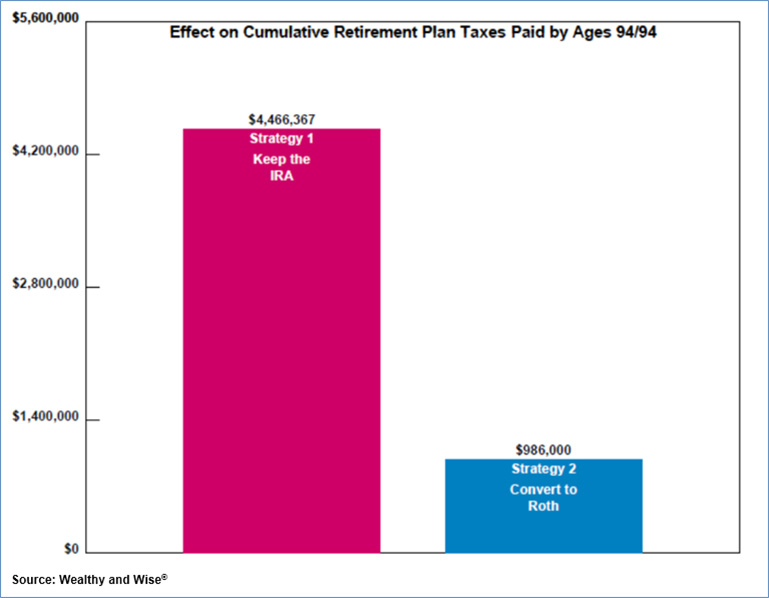

Suppose in ten years the Democrats control of the House, Senate, and Presidency. They have promised to raise the top income tax rate, and they do so by increasing it to 75% just as Kerry and Amanda retire at age 70. The graphic below shows the tax consequences to their IRA / Roth IRA comparison.

| Image 3 |

| 49.3% Income Tax Bracket Increasing to 75% at Age 70 |

| Strategy 1: Keep the IRA |

| vs. |

| Strategy 2: Convert to a Roth |

Overall taxes on the IRA have increased from $2,935,893 as shown in Image 1 to $4,466,367, a 52% escalation. The income tax on the Roth is unaffected having taken place at their age 60 in 2018. If you expect income tax rates to rise anytime in the future, it is a seriously good idea to do a Roth conversion as soon as possible, particularly if you can bury the tax by way of an asset withdrawal and improve net worth in the process.

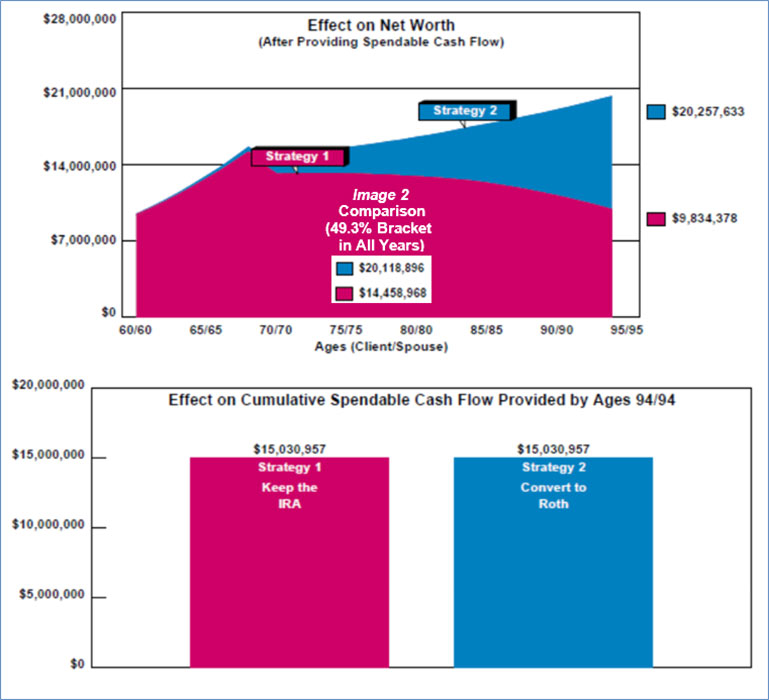

You can see the effect on net worth below.

| Image 4 |

| 49.3% Tax Bracket Increasing to 75% at Age 70 |

| Strategy 1: Keep the IRA |

| vs. |

| Strategy 2: Convert to a Roth |

The increased tax bracket reduces the long-range net worth of Strategy 1 by $4,624,590 (a 32% decrease). The overall gain in Strategy 2 has grown to $10,423,255, 106% greater than Strategy 1, solely because of the Roth conversion.

In the O’Neills’ marginal tax bracket of 49.3% changing to 75% at age 70, they would have to earn an annual, pre-tax, compounded rate of return of 10.219% for ten years increasing to 15.349% thereafter to turn $966,000 into $10,423,255 over 35 years.

Click here to see the proof of the annual, pre-tax, compounded rate of return required to produce the gain in net worth indicated for Strategy 2 in Image 2 and Image 4.

Now tell me: Can income tax ever be a good investment? You bet it can, and a Roth conversion proves it!

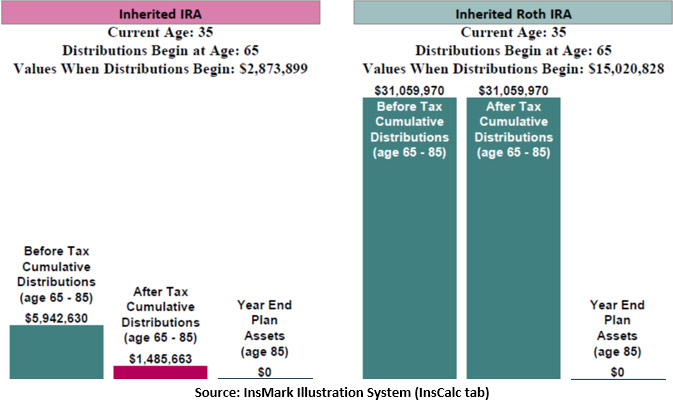

Inherited IRA vs. Inherited Roth IRA

There is another significant aspect of this analysis involving a potential inheritance alternative that Kerry and Amanda can provide for their daughter, Erin, currently age 30.

For this evaluation, let’s assume that Erin inherits either the IRA or the Roth at her age 65, 35 years hence. Erin will pay taxes on distributions from the inherited IRA. The Roth is not taxed at all.

Examine the enormous cash flow difference for Erin between the inherited IRA and the inherited Roth in Image 5.

| Image 5 |

| Comparison of Inherited IRAs |

| for Erin O’Neill at Age 65 |

| (Erin is currently age 30) |

The Roth conversion not only adds $10,423,255 to Kerry and Amanda’s long-range net worth (see Image 1), it also adds an additional $29,574,307 ($31,059,870 minus $1,485,663) to their daughter’s after tax, retirement cash flow. The $966,000 tax cost generated by the Roth conversion is not just a good investment as noted above – it is an outstanding one for this family!

Click here to review the reports that confirm the numbers in Image 5. (The bar graph in Image 5 appears at the bottom of Page 1 of the Preface.)

The next time you have parents considering a Roth conversion, be sure to bring the issue of an inherited IRA vs. an inherited Roth to their attention as it is certainly a showstopper. The impact on heirs of an inherited Roth makes the original decision to convert to a Roth virtually irresistible.

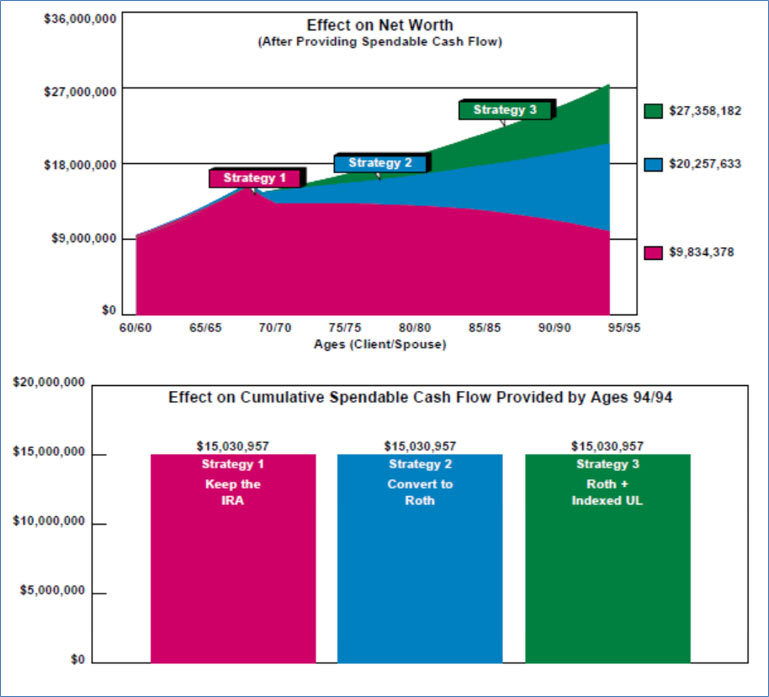

Strategy 3

Let’s introduce some Indexed Universal Life (IUL) into the retirement plan with its cost funded by withdrawals from assets just like the income tax cost of the Roth conversion.

Policy features for Strategy 3 are:

- Death benefit1: $3,824,663;

- Premiums: $300,000 for ten years funded by asset allocation;

- Annual policy loans starting in year 11: $350,000.

- 1Increasing for 10 years; level thereafter. The face amount is reduced in year 11 to the minimum required to avoid MEC classification as well as maximize cash value and cash flow.

Click here to review the life insurance illustration.

The graphic below shows the results of the integration of the life insurance policy’s costs and values into the O’Neills’ wealth analysis.

| Image 6 |

| 49.3% Tax Bracket Increasing to 75% at Age 70 |

| Strategy 1: Keep the IRA |

| vs. |

| Strategy 2: Convert to a Roth |

| vs. |

| Strategy 3: Add Indexed Universal Life |

Strategy 3 adds $7.1 million more in long-range net worth while still maintaining the desired retirement cash flow.

Click here to review the entire Wealthy and Wise evaluation summarized in Image 6. (Highlights of the impressive results to heirs are on Page 3.) There are 80 pages of graphics and numbers. The system backs up every one, and you’ll never know when you’ll need to answer this inevitable question from an adviser, “Where did this number come from?” That’s why I provide access to all of them for you in my Blogs as well as the Digital Workbook Files that created them (see below).

Most Wealthy and Wise users select a few pivotal illustrations for the main report and put the balance in supplemental sections or an Appendix. More elaborate report organization can be accomplished (Table of Contents and Section pages) through use of the following prompt -- which I used for this Blog -- located on the bottom right of the Main Workbook Window:

Conclusion

The combination of a Roth conversion, an Inherited Roth IRA, and IUL produces remarkable results, and Wealthy and Wise is a superb platform for the analysis.

Sometimes income tax can be a good investment – for Kerry, Amanda, and Erin, it’s an extraordinary one.

Licensing InsMark Systems

To license Wealthy and Wise and the InsMark Illustration System, visit us online or contact Julie Nayeri at Julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President — Sales, at dag@insmark.com or (925) 543-0513.

Creating Similar Presentations

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

Digital Workbook Files For This Blog

New Zip File Downloaders

Watch the video.

Digital Workbook Files For This Blog

Experienced Zip File Downloaders Download the zip file, open it, and double click the Workbook file name to open it in your InsMark System.

|

Before downloading and reviewing any files, be certain you have installed the most current updates to your Wealthy and Wise and InsMark Illustration System. Do this using Live Update available under Help on the main menu bar of the System or this icon on the main menu bar:

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark Systems. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

If you obtain the digital workbook for Blog #176, Click here for a guide to its content. It will be invaluable to you.

InsMark’s Referral Resources

(Put our Illustration Experts to Work for Your Practice)

We created Referral Resources to deliver a “do-it-for-me” illustration service in a way that makes sense for your practice. You can utilize your choice of insurance company, there is no commission split, and you don’t have to change any current relationships. They are very familiar with running InsMark software.

Please mention my name when you talk to a Referral Resource as they have promised to take special care of my readers. My only request is this: if a Referral Resource helps you get the sale, place at least that case through them; otherwise, you will be taking unfair advantage of their generous offer to InsMark licensees.

Save time and get results with any InsMark illustration. Contact:

- Ben Nevejans, President of LifePro Financial Services in San Diego, CA.

![]()

Testimonials

“InsMark has created without question the best suite of software for our industry that has ever existed. I personally have been using their software for almost 30 years, and it changed my career. This unique and user friendly software will add many thousands to your income for as long as you’re in business. InsMark makes me look good, and it will you as well.”

Simon Singer, CFP®, CAP®, RFC®, Past President International Forum, InsMark Platinum Power Producer®, Encino, CA

“InsMark has increased my production by 10 fold. It clearly communicates to the client the best financial scenario to take.”

Gary Sipos, M.B.A., A.I.F.® InsMark Platinum Power Producer®, Sipos Insurance Services, Freehold, NJ

“The InsMark software is indispensable to my entire planning process because it enables me to show my clients that inaction has a price tag. I can’t afford to go without it!”

David McKnight, Author of The Power of Zero, InsMark Gold Power Producer®, Grafton, WI

“Wealthy and Wise” and “InsMark” are registered trademarks of InsMark, Inc.

Important Note #1: The hypothetical values associated with this Blog assume the nonguaranteed values shown continue in all years. This is not likely, and actual results may be more or less favorable. Life insurance illustrations are not valid unless accompanied by a basic illustration from the issuing life insurance company.

Important Note #2: The information in this Blog is for educational purposes only. In all cases, the approval of a client’s legal and tax advisers must be secured regarding the implementation or modification of any planning technique as well as the applicability and consequences of new cases, rulings, or legislation upon existing or impending plans.

Important Note #3: Many of you are rightly concerned about the potential tax bomb in life insurance that can accidentally be triggered by a careless policyowner when policy loans are present and net cash values are so low that the income tax on the gain on surrender (calculated using gross cash values less basis) is more – often significantly more – than the net cash surrender value.

This lurking tax bomb can be present in all forms of whole life and universal life where policy loans of any type are utilized. It can be avoided, and you, the producer, are key to making sure your clients are aware of how to sidestep it.

A tax bomb can be avoided if the policy is neither surrendered nor allowed to lapse, since the policy death benefit wipes away the income tax liability. The foundation of this special treatment is IRC Section 101. This statute provides that the proceeds of life insurance maturing as a death claim are exempt from federal income tax. This applies to the full death benefit, including any cash value component whether loans exist or not.

Can your clients remember these facts years into the future? If they are incapacitated, will family members understand the issues? It is probably best to file a short note with the policy – something like this (although your compliance officer will likely have preferred language):

If/when you take policy loans on this policy, be sure to talk to your financial adviser before surrendering or lapsing the policy in order to anticipate unexpected tax consequences that may otherwise be avoided.

Does this note make it harder or easier to deliver the policy? It’s harder if you haven’t discussed it with your client; easier if you have. And that’s the point – you should discuss it.

Some life insurance companies have concierge units that monitor loan status at the point of lapse or surrender, and you would be well-advised to select an insurance company with this capacity. To be effective regarding the tax bomb, such carriers need to be proactive in their client relationships, not merely reactive to client inquiries. I hope that ultimately the policyholder service division of all life insurance companies will bring this potential liability to the attention of those surrendering or lapsing policies, particularly those policies with 50% or more of the gross cash value subject to outstanding loans.

![]()

More Recent Blogs:

Blog #175: Best Way to Evaluate Roth Conversions (Part 1 of 2)

Blog #173: The Impact of Tax Reform on Retirement and Estate Planning Presentations

Blog #17#: Arbitrage vs. Accelerated Arbitrage™ (Part 2 of 2)

Blog #171: Arbitrage vs. Accelerated Arbitrage™ (Part 1 of 2)

| 3 Reasons Why It’s Profitable For You To Share These |

| Blog Posts With Your Business Associates and |

| Professional Study Groups (i.e. “LinkedIn”) |

Robert B. Ritter, Jr. Blog Archive