(Click here for Blog Archive)

(Click here for Blog Index)

(Presentations in this blog were created using the InsMark Illustration System and Wealthy and Wise®)

|

Note from Bob: Blog #168 (Part 1) is the beginning of a study that deals with some principles involving the disadvantages of tax deferred retirement plans and its tax deferred cousin, deferred annuities. Part 2 (Blog #169), due out in early October, will include a comprehensive retirement study that includes the logic presented below. Design details of this two-part evaluation are included as a main topic in the 2018 InsMark Symposium scheduled for March 2 – 3, 2017, in Las Vegas. Click here for Symposium details, the Agenda, and registration information. |

Background

Imagine you own a business with another person. You put in 60% of the risk capital and your partner contributes 40%. Since then, you have done all the work.

Unfortunately, while your partner currently owns about 40% of the business, your partnership agreement allows your partner to increase its percentage ownership of the business at any time to whatever it wants. Moreover, you have no right to question, protest, or appeal this decision.

To make matters worse, your business partner is in serious financial trouble and is deeply in debt to creditors, many of whom are issuing threats about the ever increasing debt load. And, even with these threats from creditors, your business partner continues its lavish spending. Finally, your partner uses troubling language during meetings and talks about “how much of the business you will be allowed to keep” rather than recognizing you as the owner and primary driver of the business and its market value.

As that business owner, you would be more than worried.

Welcome to the world of those with money in deductible retirement plans (close to $24 trillion and counting), i.e., IRA, 401(k), 403(b), Keogh, Sec. 457, profit sharing plans, etc., all sharing their assets with the Hidden Partner’s tax collection department, the Internal Revenue Service.

Blog #166 and Blog #167 are both devoted to exposing the impact of income taxes on the retirement income developed from such plans versus the tax free cash flow that can be generated from private retirement plans funded with 21st century cash value life insurance.

It is not just a retirement cash flow issue. An appropriate wealth evaluation must also include a comprehensive analysis of the impact of that cash flow on net worth and wealth to heirs.

The accumulating values of both tax deferred retirement plans and tax deferred accounts (like deferred annuities) show unrealistic values since the deferred income tax present in both are included in net worth. It is surprising that banks, federal and state regulators, and CPAs issuing audited statements allow its inclusion as there is no way to avoid the tax. Including it as part of a net worth statement produces unrealistic and misleading valuations. (At the very least, it is a contingent liability.)

To measure and compare these Hidden Partner issues, let’s look at a Solo 401(k), a plan for self-employed individuals and owner-only businesses.

Contribution Limits for a Solo 401(k)

An eligible employee can stash away as much as $18,000. The company can contribute an additional 25% of compensation up to a maximum of $54,000, including the employee contribution – and $6,000 more if age 50 or older. The amount can double if a spouse is also employed. These contributions are discretionary, so the maximum can be saved in flush years and nothing in tougher times.

Below is a summary of the individual Solo 401(k) plan limits for 2017:

| 401(k) Elective Deferrals | $18,000 |

| Annual Defined Contribution Limit | $54,000 |

| Catch-Up Contribution Limit1 | $6,000 |

| Maximum Contribution | $60,000 |

| Qualifying Spouse Maximum Contribution | $60,000 |

| Total Both Qualifying Spouses | $120,000 |

1Employees age 50 and over.

Case Study (both doctors are in the same practice)

- Wayne Rawlings, MD: Orthopedic Surgeon, age 50

- Lauren Rawlings, MD: Anesthesiologist, age 50

- Retirement age: 70

- Marginal tax bracket: 39.6%

- Plan: Solo 401(k) for each – assumed yield: 7.00% (1.00% mgt. fee)

- Contribution: $60,000 each ($54,000 plus $6,000 catch-up)

- Annual after tax cost of each Solo 401(k): $36,420

- Total after tax cost of both Solo 401(k)s: $72,840

|

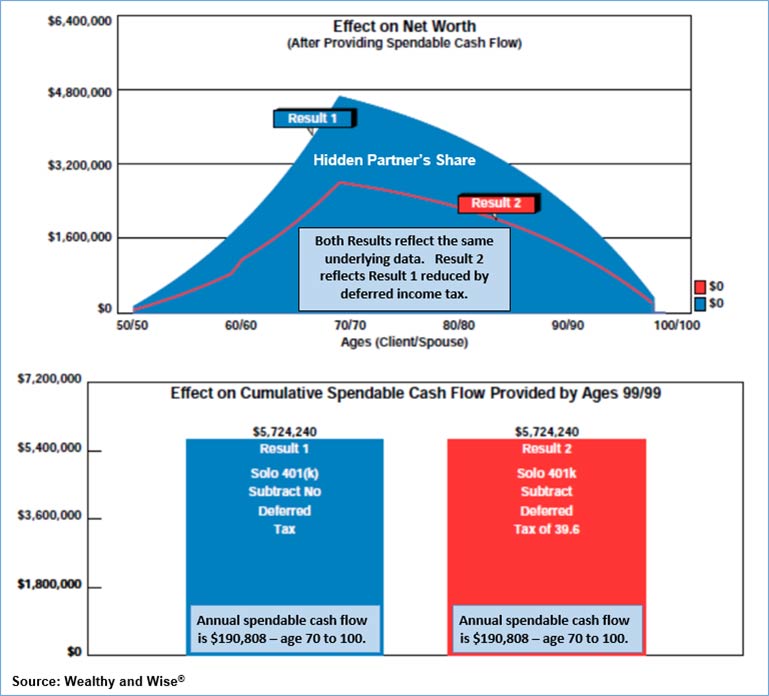

Wayne and Lauren’s joint life expectancy is age 90, and they want to include an additional ten years in the analysis as a safety valve. Using the assumptions above, if they each withdraw a level amount of $157,954 starting at age 70, each 401(k) will last for 30 years – until age 100. After the assumed 39.60% income tax allocation for their Hidden Partner, this will produce $190,808 in annual after tax funds ($157,954 x 2) x (1- .396). At age 100, both 401(k)s are exhausted. |

|

See below for the impact of the Hidden Partner on both 401(k)s. There is no difference in after tax cash flow as both accounts assume a 39.60% tax bracket on the same withdrawal pattern.

| Image 1 |

| Hidden Partner’s Effect on Net Worth |

As the text box in the graphic indicates, an optional new feature in Wealthy and Wise reduces Result 2 by the portion of retirement assets representing income tax still due on Result 1. Is it fair to illustrate a retirement account this way? If you can’t withdraw a dollar without paying income tax in your top marginal bracket, shouldn’t that grab by the Hidden Partner be reflected in the account valuation?

Long-range, there is no difference; they both end up at $0, but try convincing a client that short- and interim-term net worth is not important. That said, you can elect not to utilize this new feature in Wealthy and Wise; however, I will reflect it throughout this Blog as well as most future Blogs.

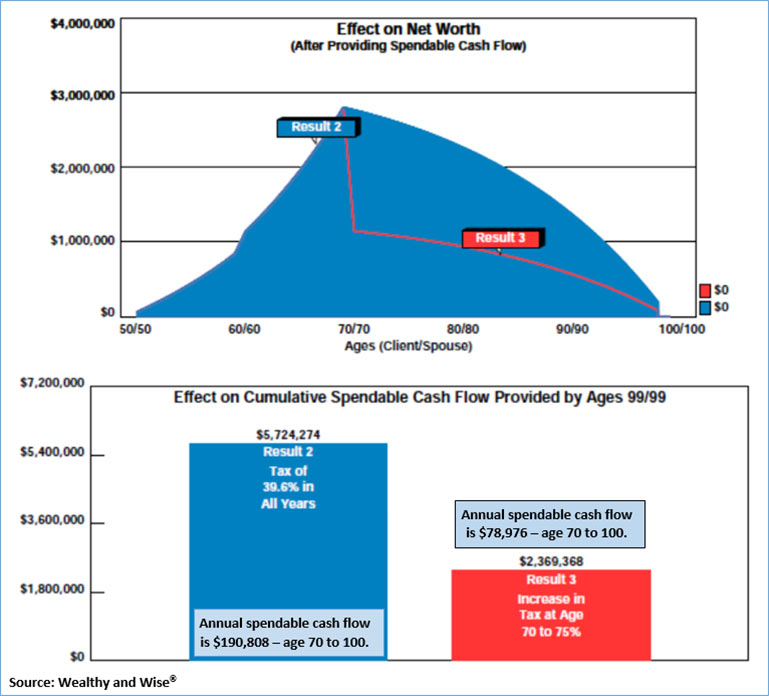

A Nasty Alternative

With the Hidden Partner’s insatiable appetite for tax revenue to fund skyrocketing expenditures and national debt, income tax brackets could increase considerably. Unless you see something on the horizon that I don’t, they undoubtedly will.

What is your perspective on long-range income tax rates? Mine is that much higher tax rates are inevitable due to the Hidden Partner’s profligate ways. Click here to review the history of the top income tax rates. How high could they go – who knows? But they once were at 94%, so let’s test out a 75% bracket occurring at the Rawlings’ age 70.

| Image 2 |

| Hidden Partner’s Effect on Retirement Plans |

Increased income taxes have an extraordinarily nasty effect on Result 3 where spendable cash flow is only 41% of Result 2.

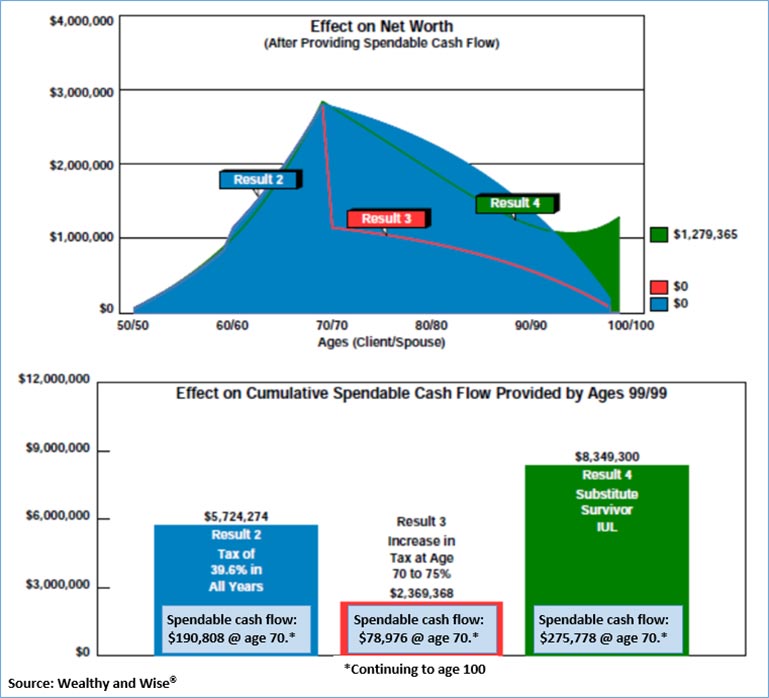

Let’s next introduce cash value life insurance into the evaluation:

- Indexed survivor universal life at 7.00%;

- Face amount: $1,882,151 (incr. for 20 years; then level);

- Premium: $72,400 for 20 years;

- Click here to review the policy illustration.

Below are the Wealthy and Wise comparative results after importing the policy values. (All of the cash flow and net worth of Result 4 consists of life insurance cash values and participating loans which means, of course, that the Hidden Partner’s tax bite has been eliminated in Result 4.)

| Image 3 |

| Hidden Partner’s Effect on Retirement Plans |

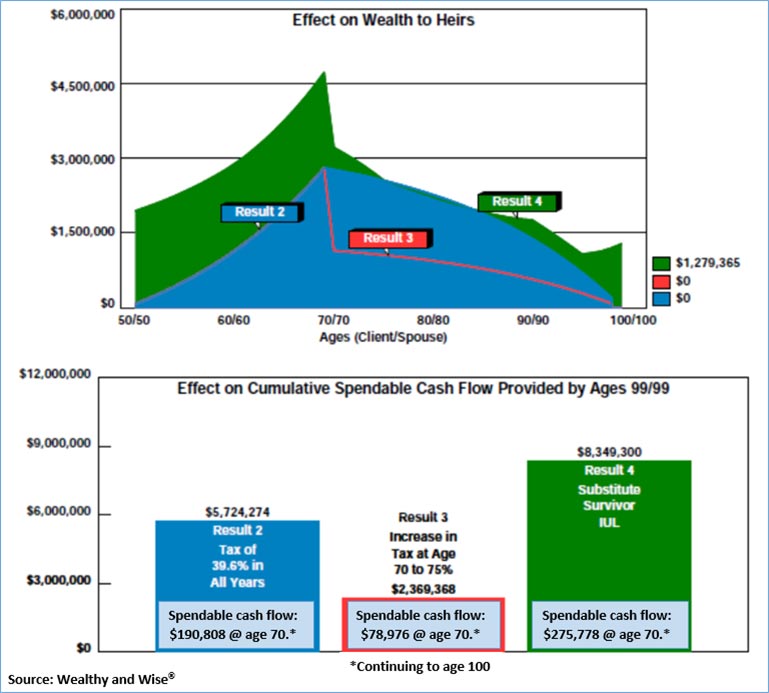

As you can see below, the effect on wealth to heirs is further enhanced with the substitution of indexed survivor universal life in Result 4:

| Image 4 |

| Hidden Partner’s Effect on Wealth to Heirs |

Click here to view the 50-page Wealthy and Wise evaluation. That’s not as tedious as you may think as most of the numerical reports run to two pages due to the 50 years in the analysis; however, a comprehensive evaluation like this does require some detail. I don’t know how you can present it professionally without revealing all its components, and I recommend that you have all the reports for a given analysis with you when you are visiting with a client or client’s attorney or CPA. The system backs up every number shown, and you never know which report you’ll need to have handy to answer the inevitable question, “Where did this number come from?”

Most Wealthy and Wise users select a few key illustrations for the main report and put the balance in supplemental sections or an Appendix. More elaborate report organization can be accomplished (Table of Contents and Section pages) through use of the following prompt which I used for this Blog — located on the bottom right of the Main Workbook Window:

Conclusion

Government-sponsored plans cannot compete with, in this case, indexed survivor universal life. It is not even close. The results would have been equally as good had I used individual indexed universal life policies on Wayne and Lauren.

The reason I used the survivor variation is because, if I used a single life policy on, say, Wayne, and he died unexpectedly, let’s say at age 85, the power of the arbitrage produced by accumulated participating loans on his policy would die with him. Lauren would receive a policy death benefit, but it would not be nearly enough to sustain the same after cash flow from the policy had Wayne not died. (The reverse is true if Lauren were the insured.) By using a survivor policy, if one death occurs, the policy continues its arbitrage effectiveness producing significant levels of after tax policy participating loans. A survivor policy is the most effective way to accomplish this.

Bill Boersma quote: “I can only wonder if another asset with the same qualities would be implemented more frequently if it wasn’t called life insurance.”

Using an indexed life insurance policy typically means either (a) more net worth and wealth to heirs or (b) more spendable cash flow, any of which can usually be produced with no increase in contributions due to the tax defectiveness of formal retirement plans as noted above. Any client that eliminates cash value life insurance as a funding resource for retirement cash flow is effectively saying, “I don’t mind inefficient retirement planning.” And this logic applies to any deductible retirement plan. It even applies to Roths as described in Blog #167.

InsMark illustrations can also assist you with some aspects of your DOL compliance since, when appropriate, the calculations show that you are acting in the client’s best interest in recommending cash value life insurance as a supplemental, retirement savings alternative.

Below are additional advantages when life insurance is used:

- There are no federally mandated limits to premiums for life insurance, and once this is understood, many clients will increase their funding for the life insurance;

- A waiver of premium can be attached to life insurance in the event of disability;

- Tax free cash flow from the life insurance (withdrawals to basis and/or loans) can be accessed prior to age 59 1/2 with no premature distribution tax;

- Life insurance also provides a significant death benefit ($1,882,151 of second-to-die coverage for Wayne and Lauren).

- Many policies allow for advance of death benefits to fund long term care costs.

There is one way in which government-sponsored retirement plans have an advantage over the cash value life insurance alternatives. In most cases, government plan assets are creditor proof. See the attached state-by-state listing1 of creditor-proof opportunities from Duggan Bertsch, a Chicago law firm that specializes in a wide range of wealth planning. The list includes the states that protect cash values of life insurance from creditors.

1InsMark makes no guarantee or warranty of the list’s accuracy. Contact Duggan Bertsch directly with fee-based requests for additional information.

Note: I added one last comparison in the Wealthy and Wise digital Workbook file available below. In it, I compared reducing the income tax bracket to 25% in all years to address the skeptical reader who may believe a Trump-type tax decrease could last forever (not an opinion in which I concur due to the spending patterns of both political parties). The indexed survivor universal life still ends up as the superior purchase producing more than $1,200,000 of both additional after tax retirement cash flow and long-range net worth. This illustration is not included with this Blog, but you can review it in the Wealthy and Wise digital Workbook available below.

Next Up

In order to demonstrate the invasive nature of income tax on deductible retirement plans, this Blog has compared only Wayne and Lauren’s retirement savings, not their overall assets and retirement objectives. In Blog #169: The Hidden Partner (Part 2 of 2) due for posting in early October, I will integrate the principles established in this Blog to complete a retirement plan for them. The comparative results will stun you.

Files For This Blog

New Zip File Downloaders

Watch the video.

Experienced Zip File Downloaders Download the zip file, open it, and double click the Workbook file name to open it in your InsMark System.

|

Before downloading and reviewing any files, be certain you have installed the most current update to your Wealthy and Wise System, otherwise you will miss several new enhancements which are outlined in this Blog. Do this using Live Update available under Help on the main menu bar of the System or this icon on the main menu bar:

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark Systems. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

If you obtain the digital workbook for Blog #168, click here for a guide to the content. It will be invaluable to you.

Licensing InsMark Systems

To license any of the InsMark software products, visit our Product Center online or contact Julie Nayeri at Julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President — Sales, at dag@insmark.com or (925) 543-0513.

For help on how to use InsMark software, go to The Quickest Way To Learn InsMark.

InsMark’s Referral Resources

(Put our Illustration Experts to Work for Your Practice)

We created Referral Resources to deliver a “do-it-for-me” illustration service in a way that makes sense for your practice. You can utilize your choice of insurance company, there is no commission split, and you don’t have to change any current relationships. They are very familiar with running InsMark software.

Please mention my name when you talk to a Referral Resource as they have promised to take special care of my readers. My only request is this: if a Referral Resource helps you get the sale, place at least that case through them; otherwise, you will be taking unfair advantage of their generous offer to InsMark licensees.

Save time and get results with any InsMark illustration. Contact:

- Ben Nevejans, President of LifePro Financial Services in San Diego, CA.

Testimonials

“InsMark has increased my production by 10 fold. It clearly communicates to the client the best financial scenario to take.”

Gary Sipos, M.B.A., A.I.F.® InsMark Platinum Power Producer®, Sipos Insurance Services, Freehold, NJ

“Major cases we are developing have all moved along successfully because of the sublime simplicity and communication capability of Wealthy and Wise. I guarantee that the proper use of this tool will dramatically raise the professional and personal self-image of any associate who dares to take the time to understand it . . .”

Phillip Barnhill, CLU, InsMark Gold Power Producer®, Minneapolis, MN

“InsMark is the Picasso of the financial services world — their marketing savvy never fails to amaze me.”

Doug Peete, Past President, Top of the Table, InsMark Silver Power Producer®, Overland Park, KS

Important Note #1: The hypothetical values associated with this Blog assume the nonguaranteed values shown continue in all years. This is not likely, and actual results may be more or less favorable. Life insurance illustrations are not valid unless accompanied by a basic illustration from the issuing life insurance company.

Important Note #2: Many of you are rightly concerned about the potential tax bomb in life insurance that can accidentally be triggered by a careless policyowner when policy loans are present. Click here to read Blog #51: Avoiding the Tax Bomb in Life Insurance.

Important Note #3: The information in this Blog is for educational purposes only. In all cases, the approval of a client’s legal and tax advisers must be secured regarding the implementation or modification of any planning technique as well as the applicability and consequences of new cases, rulings, or legislation upon existing or impending plans.

“InsMark” and “Wealthy and Wise” are registered trademarks of InsMark, Inc.

![]()

More Recent Blogs:

Blog #167: The Retirement Cost of Ignoring Life Insurance (Part 2 of 2)

Blog #166: The Retirement Cost of Ignoring Life Insurance (Part 1 of 2)

Blog #165: Lobsters for Retirement

Blog #164: Family Net Worth (It’s Irresistible!) Part 2 of 2

Blog #163: Family Net Worth (It’s Irresistible!) Part 1 of 2

| 3 Reasons Why It’s Profitable For You To Share These |

| Blog Posts With Your Business Associates and |

| Professional Study Groups (i.e. “LinkedIn”) |

Robert B. Ritter, Jr. Blog Archive

You’re more brilliant than ever, Mr. Ritter. Hope your health continues to be perfect for many years to come. Your friend, Wayne.

Thanks for that super compliment, Wayne.

Bob Ritter

InsMark President