(Click here for Blog Archive)

(Click here for Blog Index)

(Presentations in this blog were created using the InsMark Illustration System)

Recently in Blog #142: Increased Taxes Are Coming, I compared how various changes in income tax brackets significantly reflect how investments perform compared to well-designed, personally- or business-owned cash value life insurance due to its non-correlation with changes in income tax rates.

The analysis in Blog #142 compared indexed universal life (“IUL”) at 7.00% to a taxable account at 7.00%, a tax deferred account at 7.00%, and an equity account with 7.00% growth and a 2.00% dividend.

Note: The indexes available for indexed universal life generally don’t credit a dividend. The current S&P 500 dividend yield is about 2.00%. So to be fair, I added a 2.00% dividend to the equity account for a gross yield of 9.00%, 200 basis points greater than the IUL.

The contributions to those three accounts ($25,000 for 20 years) were identical to the premiums of the IUL. I then matched the after tax retirement cash flow from the IUL of $100,000 a year (using participating loans) starting at age 65 with the same level of after tax cash flow from the alternative accounts.

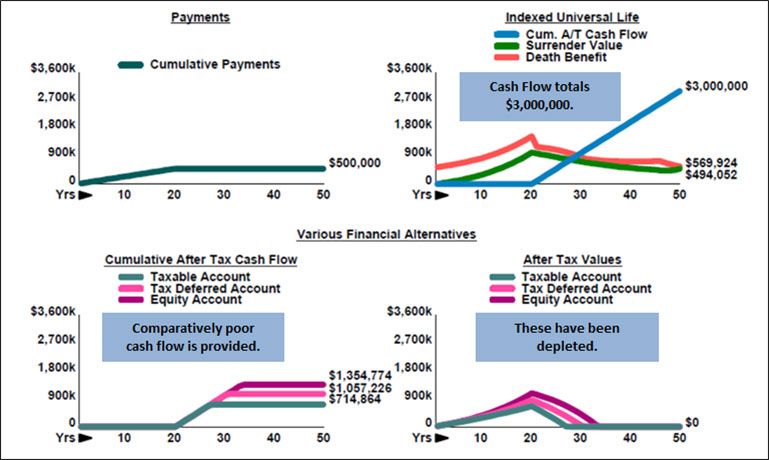

The alternatives did not fare well. Below is a graphic from Blog #142 showing the poor performance.

| Various Financial Alternatives |

| (Stable Income Tax Rates) |

| Image 1 |

Notice that all three of the alternative accounts collapse within just a few years of retirement. The best of the alternatives is the equity account although it is barely 45% of the IUL. It would need a yield of 11.14% (9.14% growth plus the 2.00% dividend) to match the IUL.

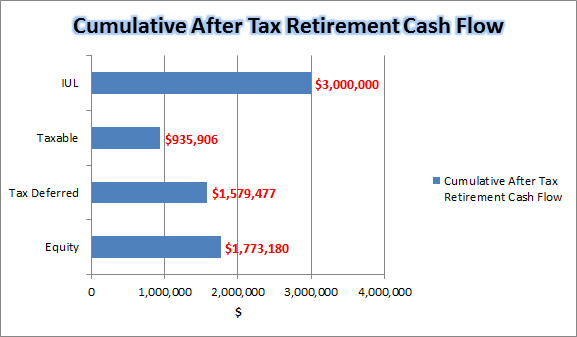

One of my good friends, Simon Singer, asked me recently why didn’t I compare a reduced level of the cash flow from the alternatives lasting as long as the cash flow from the IUL. Simon is one of the smartest financial professionals I know, so below is a look at his suggestion.

Here are the comparative results of this evaluation when level, after tax cash flow from each alternative is calculated to last from age 65 through age 100:

- IUL produces $100,000 a year (total: $3,000,000) ending up with residual cash value of $494,052.

- Taxable account produces $31,196 a year (total: $935,906) ending up with residual cash of $0.

- Tax deferred account produces $52,648 a year (total: $1,579,477) ending up with residual cash of $0.

- Equity account produces $59,106 a year (total: $1,773,180) ending up with residual cash of $43.

Note: Rounding produces some minor anomalies of the totals.

I was unable to use our popular Various Financial Alternatives (“VFA”) module for this analysis as I did in Blog #142 because VFA is designed so that the cash flow from the alternatives matches the cash flow from the IUL for as long as possible. For this Blog, I used the Illustration of Values module for the IUL, and the respective InsCalc calculators from the InsMark Illustration System (located on the InsCalc tab) for the alternatives. I put them all into one 19-page illustration entitled Don’t Burn the Nest Egg® using the following selection on the lower right side of the Workbook Main Window. (This selection helps you create a Table of Contents and Section pages.)

Click here to review Don’t Burn the Nest Egg®.

Conclusion

I am once again reminded of Bill Boersma’s comment in his article in the December 2014 issue of Trusts & Estates in which he discusses life insurance as an asset class: “I can only wonder if another asset with the same qualities would be implemented more frequently if it wasn’t called life insurance.”

InsMark’s Digital Workbook Files

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

New Zip File Downloaders

Watch the video.

Experienced Zip File Downloaders Download the zip file, open it, and double click the Workbook file name to open it in your InsMark System.

|

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark System. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

If you obtain the digital workbook for Blog #144, Click here for a Guide to each of the illustrations.

Licensing InsMark Systems

To license any of the InsMark software products, visit our Product Center online at or contact Julie Nayeri at Julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President – Sales, at dag@insmark.com or (925) 543-0513.

For help on how to use InsMark software, go to The Quickest Way To Learn InsMark.

InsMark’s Referral Resources

(Put our Illustration Experts to Work for Your Practice)

We created Referral Resources to deliver a “do-it-for-me” illustration service in a way that makes sense for your practice. You can utilize your choice of insurance company, there is no commission split, and you don’t have to change any current relationships. They are very familiar with running InsMark software.

Please mention my name when you talk to a Referral Resource as they have promised to take special care of my readers. My only request is this: if a Referral Resource helps you get the sale, place at least that case through them; otherwise, you will be taking unfair advantage of their generous offer to InsMark licensees.

Save time and get results with any InsMark illustration. Contact:

- Ben Nevejans, President of LifePro Financial Services in San Diego, CA.

Testimonials

“The InsMark software is indispensable to my entire planning process because it enables me to show my clients that inaction has a price tag. I can’t afford to go without it!”

David McKnight, Author of The Power of Zero, InsMark Gold Power Producer®, Grafton, WI

“The reason I use InsMark products is because they are so good at explaining financial concepts to all three parties: 1) the producer trying to explain the idea; 2) the computer technician trying to illustrate it; 3) the customer trying to understand it.”

Rich Linsday, CLU, AEP, ChFC, InsMark Power Producer®, Top of the Table, International Forum, Pasadena, CA

“InsMark’s Checkmate® Selling strategy is still one of the most compelling tools to bring a client to a definitive decision, based on their best case alternatives!!! Solid mathematical comparisons that prove the validity of our insurance solution!!!”

Frank Dunaway, III, CLU, Legacy Advisory Services, Carthage, MO

Important Note #1: The hypothetical life insurance illustration associated with this Blog assumes the nonguaranteed values shown continue in all years. This is not likely, and actual results may be more or less favorable. Actual illustrations are not valid unless accompanied by a basic illustration from the issuing life insurance company.

Important Note #2: Many of you are rightly concerned about the potential tax bomb in life insurance that can accidentally be triggered by a careless policyowner. Click here to read Blog #51: Avoiding the Tax Bomb in Life Insurance.

Important Note #3: The information in this Blog is for educational purposes only. In all cases, the approval of a client’s legal and tax advisers must be secured regarding the implementation or modification of any planning technique as well as the applicability and consequences of new cases, rulings, or legislation upon existing or impending plans.

“InsMark” and “Don’t Burn the Nest Egg” are registered trademarks of InsMark, Inc.

![]()

More Recent Blogs:

Blog #143: Premium Financing Opportunities In The Small Case Market

Blog #142: Increased Taxes Are Coming

Blog #141: Strategic Philanthropy

Blog #140: Zero Taxes for Social Security - InsMark Style

Blog #139: Finding Clients For Large Case Premium Financing… JUST GOT EASIER

| 3 Reasons Why It’s Profitable For You To Share These |

| Blog Posts With Your Business Associates and |

| Professional Study Groups (i.e. “LinkedIn”) |

Robert B. Ritter, Jr. Blog Archive