(Click here for Blog Archive)

(Click here for Blog Index)

(Presentations in this blog were created using the InsMark Illustration System.)

Recently, I read an article in Forbes that examines the fees associated with mutual funds, and the results were surprising. Below are the fees discussed in the article (click on the title of the table for a link to the article):

| The Real Cost of Owning a Mutual Fund* |

| *Article published in Forbes (4/04/2011). |

I typically include 1.00% or less for adviser fees in my illustrations when comparing Indexed Universal Life (IUL) to an equity account, but 4.17% in addition to that — really? According to Forbes, 4.17% is an accurate representation ignoring any advisor fees charged by a qualified broker. Let’s test the difference between a fee of 1.00% for the adviser and 5.00% (4.00% for the Forbes-type charges plus 1.00% for the adviser).

I typically include 1.00% or less for adviser fees in my illustrations when comparing Indexed Universal Life (IUL) to an equity account, but 4.17% in addition to that — really? According to Forbes, 4.17% is an accurate representation ignoring any advisor fees charged by a qualified broker. Let’s test the difference between a fee of 1.00% for the adviser and 5.00% (4.00% for the Forbes-type charges plus 1.00% for the adviser).

InsMark Case Study

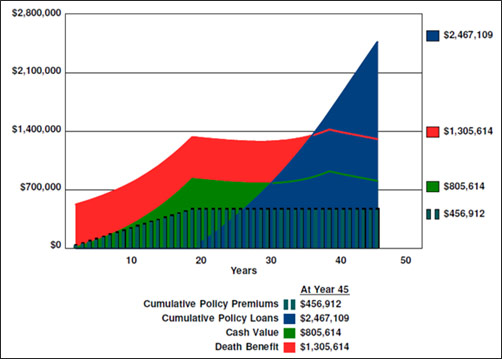

Harvey Pierce, MD, is an internist practicing in San Francisco, CA. He is considering acquiring $500,000 of additional IUL coverage.

Below is a graphic of the IUL illustration:

Click here for the full illustration.

These are nice values, but not necessarily good or bad until compared with alternatives. Most people make their best decisions in a comparative environment, so let’s do that for Dr. Pierce.

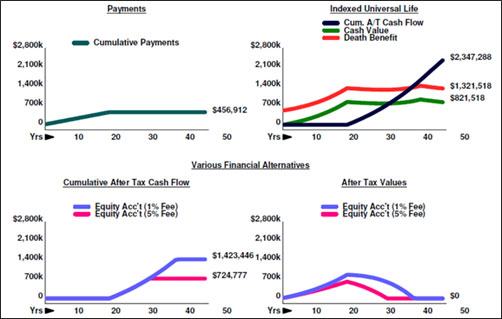

Following up with the fee discussion above, let’s compare the IUL with two equity accounts, one with a 1.00% fee for the adviser, and the other with a 5.00% fee (4.00% plus 1.00% for the adviser). Other than that, the two equity accounts are identical:

- Same deposit as the IUL;

- Same cash flow as the IUL (for as long as possible);

I used the Various Financial Alternatives module in the InsMark Illustration System for the comparison. Typically, this module does not allow you to compare two of the same accounts to the life policy; however, you can do this if you utilize the Customize investment selection and direct each to be taxed as an equity account. If you do this, be sure to name each one differently so you can tell which is which. In Dr. Pierce’s case, I used:

- Equity Acc’t (1% Fee)

- Equity Acc’t (5% Fee)

For both equity accounts, I assumed a capital gains and dividend tax rate of 30% (including a provision for state tax). I assumed a 30% turnover ratio and 60% of the growth would be subject to long-term gains; 40% short-term gains. Dr. Pierce’s 45% income tax bracket was also included.

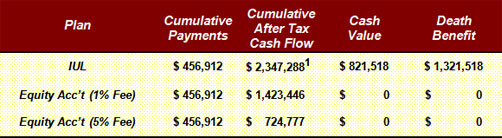

Below is a graphic of the comparative results:

| IUL vs. Equity Account |

Both equity accounts are depleted well before the final illustration year. Equity Acc’t (1% Fee) collapses in Year 37 (age 83) and Equity Acc’t (5% Fee) disappears in Year 29 (age 75).

Click here for the full illustration.

The difference in long-range values is pretty amazing:

|

Results at Age 90 |

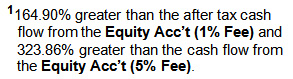

To match the cash flow and long-range cash value of the IUL, the Equity Acc’t (1% Fee) would need pre-tax equivalent growth of 10.12% plus the assumed dividend of 2.50% for a combined 12.62%. To match the cash flow and death benefit of the IUL, the Equity Acc’t (5% Fee) would need pre-tax equivalent growth of 14.82% plus the assumed dividend of 2.50% for a combined 17.32%. (You can see these numbers on Page 4 of the comparative illustration.)

Note to licensees of the InsMark Illustration System: If you want to test these growth percentages, enter them in their respective fields in the System Workbook file available below.

The equity accounts are not competitive compared to the IUL — and notice that the full $500,000 death benefit is on top of the cash value throughout the entire IUL illustration. Live or die — it’s a win/win for the IUL.

Here again is the quote from that superb article in the December 2014 issue of Trusts & Estates by Bill Boersma in which he discusses life insurance as an asset class: “I can only wonder if another asset with the same qualities would be implemented more frequently if it wasn’t called life insurance.”

Conclusion

It makes no difference if your recommended policy is a lot smaller or a lot bigger than Dr. Pierce’s, comparisons make an extraordinary difference to your clients’ understanding of the value of 21st century cash value life insurance. If you have prospects and/or clients enamored of mutual funds, the research in the Forbes’ article noted at the top of this Blog, coupled with our ability to reflect aggressive management fees in our comparisons, should provide you with some pretty serious competitive tools.

There are several comparison modules in the InsMark Illustration System that can be used in this manner:

- Other Investments vs. Your Policy (comparison to one alternative)

- Various Financial Alternatives (comparisons of up to four alternatives)

- Permanent vs. Term and a Side Fund

Comparing the policyowner’s cost of a premium financed plan with an equity account is another way this logic can be used. Similarly, the policyowner’s share of any of our benefit plans — executive bonus, leveraged executive bonus, loan-based split dollar, loan-based private split dollar, leveraged deferred compensation, and 401(k) look-alike — can be impressively compared to an equity alternative. To do this, click the following selection on the lower right of the benefit plan module while in edit mode:

This will export the policyowner’s costs and benefits of that plan to the InsMark Source Data Storage files where it can be imported into one of the three comparative modules noted above (or into Wealthy and Wise®).

InsMark’s Digital Workbook Files

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

New Zip File Downloaders

Watch the video.

Experienced Zip File Downloaders Download the zip file, open it, and double click the Workbook file name to open it in your InsMark System.

|

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark System. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

Licensing InsMark Systems

To license the Premium Financing System and/or the InsMark Illustration System, contact Julie Nayeri at julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President – Sales, at dag@insmark.com or (925) 543-0513.

InsMark’s Referral Resources

(Put our Illustration Experts to Work for Your Practice)

We created Referral Resources to deliver a “do-it-for-me” illustration service in a way that makes sense for your practice. You can utilize your choice of insurance company, there is no commission split, and you don’t have to change any current relationships. They are very familiar with running InsMark software.

Please mention my name when you talk to a Referral Resource as they have promised to take special care of my readers. My only request is this: if a Referral Resource helps you get the sale, place at least that case through them; otherwise, you will be taking unfair advantage of their generous offer to InsMark licensees.

Save time and get results with any InsMark illustration. Contact:

- Ben Nevejans, President of LifePro Financial Services in San Diego, CA.

Joint Interviews

If you want or need help from a qualified producer for joint interviews with any InsMark illustration and are willing to share the case, email us at bob@robert-b-ritter-jr.com, and we will provide you with recommendations.

Testimonials:

“The reason I use InsMark products is because they are so good at explaining financial concepts to all three parties: 1) the producer trying to explain the idea; 2) the computer technician trying to illustrate it; 3) the customer trying to understand it.”

Rich Linsday, CLU, AEP, ChFC, InsMark Power Producer®, Top of the Table, International Forum, Pasadena, CA

“Thanks to InsMark, we recently set business goals in our firm that I basically thought were ridiculously unachievable – until now.”

Brian Langford, InsMark Platinum Power Producer®, Plano, TX

Important Note #1: The hypothetical life insurance illustrations associated with this Blog assume the nonguaranteed values shown continue in all years. This is not likely, and actual results may be more or less favorable. Actual illustrations are not valid unless accompanied by a basic illustration from the issuing life insurance company.

Important Note #2: Many of you are rightly concerned about the potential tax bomb in life insurance that can accidentally be triggered by a careless policyowner. Click here to read Blog #51: Avoiding the Tax Bomb in Life Insurance.

![]()

More Recent Blogs:

Blog #99: One More Time – The Value of “You” to Your Clients

Blog #98: The Value of “You” to Your Clients (Part 2 of 2)

Blog #97: The Value of “You” to Your Clients (Part 1 of 2)

Blog #96: Retirement Cash Flow Funded by Premium Financing

Blog #95: How Much Do I Really Need?

| 3 Reasons Why It’s Profitable For You To Share These |

| Blog Posts With Your Business Associates and |

| Professional Study Groups (i.e. “LinkedIn”) |

Robert B. Ritter, Jr. Blog Archive