Laura Lake Johnson, age 35, is an established landscape painter specializing in seascapes in watercolor and oil. She has a four-year old daughter, Caroline.

As a self-employed artist, retirement planning is solely Laura’s responsibility, and she is reviewing an illustration for a cash value life insurance policy. It includes a substantial $1,000,000 death benefit to help care for Caroline should anything happen to Laura. It also illustrates almost $1,500,000 of total, after tax, retirement cash flow for Laura from her age 65 to her life expectancy of age 85.

As is typically the case, her Basic Illustration is 25 pages long, and although it includes very valuable information, it is an appalling presentation piece. What can you add to this tedious document that not only brightens the presentation but makes it more easily understood by Laura?

Click here for my suggestion. It is one of the most straightforward reports from the InsMark Illustration System: Illustration of Values. By including it as a forerunner to the Basic Illustration, communication to Laura can be significantly improved.

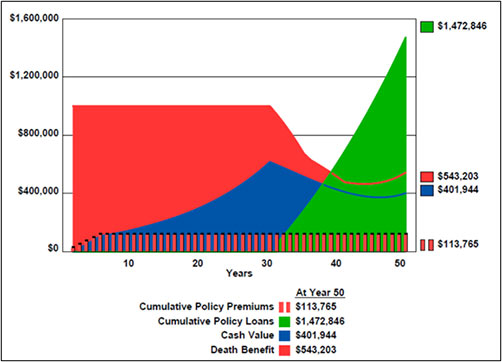

This is the key graphic from Laura’s Illustration of Values:

Do you want it even simpler? Click here for the most uncomplicated of all, Life Plan from the InsMark Illustration System.

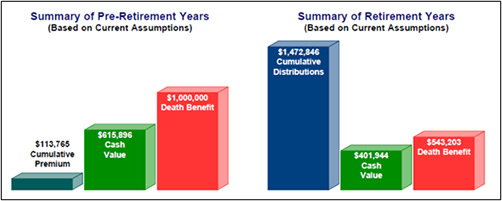

This is the key graphic from Laura’s Life Plan illustration:

We refer to our supplemental illustrations as “diet” proposals — plenty of white space with no numbers or text printing edge to edge.

I am not suggesting that you ignore Laura’s 25-page Basic Illustration — only that you disregard it as your primary presentation tool. It is complex because it serves too many masters: actuarial, legal, compliance, you — and finally, Laura.

Please understand that the purpose of InsMark is to augment the carrier’s Basic Illustration; however, our Supplemental Illustrations are not valid without this footnote (or some carrier-approved variation of it) appearing at the bottom of our numerical data:

This illustration assumes the nonguaranteed values shown continue in all years. This is not likely, and actual results may be more or less favorable. This illustration is not valid unless accompanied by a basic illustration from the issuing life insurance company.

While InsMark has plenty of advanced illustration capacity, our Supplemental Illustration formats are what has made us so popular. It is all we do, and I hope they prove useful to you.

A Little More Complex

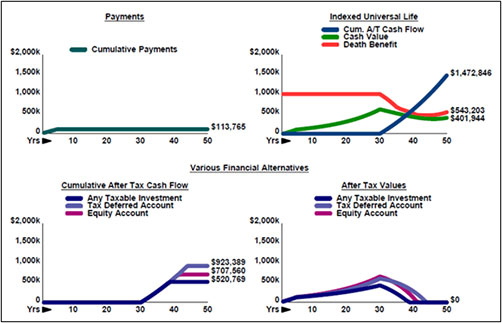

For those who prefer comparing alternative investments to the values of the life insurance, adding our popular Various Financial Alternatives produces a compelling, although more complex, presentation. You can choose from 21 different alternative investments or customize your own.

Click here to view illustrations of Various Financial Alternatives from the InsMark Illustration System. Included are a Taxable Account (7.50%), a Tax Deferred Account (7.50%), and an Equity Account (6.50% growth; 1.00% dividend).

This is the key graphic from Laura’s Various Financial Alternatives illustration:

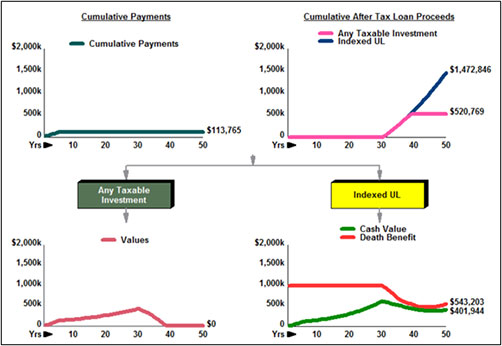

You may find the illustration from Various Financial Alternatives too busy with numbers. In this event, I recommend Other Investments vs. Your Policy from the InsMark Illustration System which compares the life policy to your selection of just one of the alternative investments.

Click here to view illustrations from Other Investments vs. Your Policy. I chose “Any Taxable Investment” at 7.50% as the alternative to the life insurance.

Below is the key graphic from Laura’s Other Investments vs. Your Policy illustration.

Important Note: Laura’s retirement cash flow in all the examples consists of participating policy loans. Many of you are rightly concerned about the potential tax bomb associated with life insurance policies with loan activity that can accidentally be triggered by a careless policyowner. Click here to read Blog #51: Avoiding the Tax Bomb in Life Insurance.

InsMark’s Digital Workbook Files

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

New Zip File Downloaders

Watch the video.

Experienced Zip File Downloaders Download the zip file, open it, and double click the Workbook file name to open it in your InsMark System.

|

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark System. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

Licensing

To license the InsMark Illustration System, contact Julie Nayeri at julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President – Sales, at dag@insmark.com or 925-543-0513.

InsMark’s Referral Resources

(Put our Illustration Experts to Work for Your Practice)

We created Referral Resources to deliver a “do-it-for-me” illustration service in a way that makes sense for your practice. You can utilize your choice of insurance company, there is no commission split, and you don’t have to change any current relationships. They are very familiar with running InsMark software.

Please mention my name when you talk to a Referral Resource as they have promised to take special care of my readers. My only request is this: if a Referral Resource helps you get the sale, place at least that case through them; otherwise, you will be taking unfair advantage of their generous offer to InsMark licensees.

Save time and get results with any InsMark illustration. Contact:

- Ben Nevejans, President of LifePro Financial Services in San Diego, CA.

Joint Interviews

If you want or need help from a qualified producer for joint interviews with any InsMark illustration and are willing to share the case, email us at bob@robert-b-ritter-jr.com, and we will provide you with recommendations.

Testimonials:

“The reason I use InsMark products is because they are so good at explaining financial concepts to all three parties: 1) the producer trying to explain the idea; 2) the computer technician trying to illustrate it; 3) the customer trying to understand it.”

Rich Linsday, CLU, AEP, ChFC, InsMark Power Producer®, Top of the Table, International Forum, Pasadena, CA

“InsMark is the Picasso of the financial services world – their marketing savvy never fails to amaze me.”

Doug Peete, Past President, Top of the Table, InsMark Silver Power Producer®, Overland Park, KS

![]()

More Recent Blogs:

Blog #82: A Great Holiday Video

Blog #81: Economics of a Roth IRA Conversion

Blog #80: Converting Low Yielding Assets into a Charitable Gift Annuity

Blog #79: Insurance Sales to Clients with IRAs

Blog #78: More on How to Smite a Termite

| 3 Reasons Why It’s Profitable For You To Share These |

| Blog Posts With Your Business Associates and |

| Professional Study Groups (i.e. “LinkedIn”) |

Robert B. Ritter, Jr. Blog Archive

Thank you for the “clear” illustration, I’m assuming that this is an add in piece to all of what is required.

When I first entered the industry back in the early 80’s we were allowed to prepare a similar summary comparing three alternatives on one page: a mutual fund, an annuity and a whole life plan. Almost 100% chose the whole life plan because it held the most benefits. Since then, these simply illustrations have been banned, probably because some idiot sold a 90 year old widow life insurance.

I made the Million Dollar roundtable several years using these and never ran into any serious issues. Only later did this way of selling get banned.

The biggest problem I have with all of this stuff that we are supposed to give the insured is that they read it once (with me) then file it away for ever….So, what purpose did it serve except to prevent a sale by making a simple idea suddenly overly complicated and therefore create a lot of distrust.

Perhaps, you have a better understanding.

ALEX

A couple of thoughts, Alex.

You are correct. The Basic illustration from the life insurance carrier must accompany our Supplemental illustration.

You may well have been using insMark way back in the 80s. We first developed our Various Financial Alternatives (VFA) in 1982. When you say banned, I think you are referring to an action by what is now known as FINRA. To my knowledge, FINRA has never banned VFA with whole life, universal life or indexed universal as the life insurance alternative in VFA. I suspect the ban you are referring to came from the internal compliance departments at the insurance company whose product you were illustrating. That has happened occasionally, but this is not the position of FINRA. We have over 60 companies licensed for our software, and the compliance folks at only one or two still ban our VFA module

That said, FINRA has never allowed VFA-type illustrations using variable universal life, and none of our linked companies allow it to be used with variable UL.

I agree with you that much of what an insured is provided with is a lot of gobbledygook designed primarily to protect the insurer. The 25+ page basic illustration has gone way beyond customer needs — in many ways like a prospectus that is rarely read.

Thanks, Alex, for taking the time to comment.

Bob Ritter

InsMark President