(Presentations were created using Wealthy and Wise®.)

Brace yourself; this is a good one!

Last week in Blog #37, we reviewed the case of Elizabeth Rand, MD, age 40, who was analyzing the purchase of $3.6 million of indexed universal life (IUL). We compared the IUL to $3.6 million of 30-year level term insurance coupled with a side fund. We also illustrated $120,000 in policy loans on the IUL beginning at Dr. Rand’s age 60. As you may recall, the IUL turned out to be the smart way to go -- by a wide margin. Click here if you would like to review her comparison of IUL to term insurance using the InsMark Illustration System.

Wealthy and Wise®, InsMark’s wealth planning system, can also perform effective term comparisons, and it goes a step beyond by evaluating and comparing the overall impact on Dr. Rand’s cash flow, net worth, and wealth to heirs.

To gauge the impact of Wealthy and Wise, let’s first review Dr. Rand’s current financial picture:

| $ 350,000 | Taxable Assets @ 5.00% |

| 350,000 | Tax Exempt Assets @ 4.00% |

| 1,500,000 | Equity Assets @ 7.50% growth; 1.00% dividend |

| 300,000 | Defined Contribution Plan Assets @ 7.50% |

| 500,000 | Residence @ 5.00% growth |

| (400,000) | Mortgage @ 4.40% |

| 100,000 | Art Collection @ 7.50% |

| 400,000 | Personal Property @ -5.00% |

| $ 3,100,000 | Total Net Worth |

Click here for comments about yields and Monte Carlo simulations.

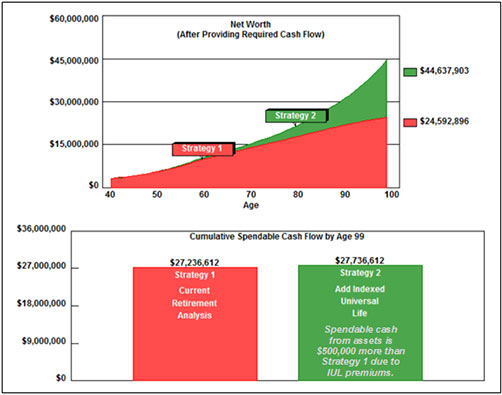

The IUL policy has five scheduled premiums of $100,000 each, and Dr. Rand does not plan to pay those premiums from her income. Rather, she will pay them by way of withdrawal from her assets as part of the Maximize Net Worth solve available in Wealthy and Wise. This will deplete her current assets by $500,000 over the next five years and replace them with the values of the IUL policy.

At her retirement age 60, Dr. Rand wants $200,000 a year in today’s dollars for after tax retirement cash flow indexed at 3.00% as an inflation offset. In this case, $200,000 in today’s dollars will need to be $361,222 in tomorrow’s dollars by her age 60, and this amount will also need to rise by 3.00% in retirement years to meet her expectations. These amounts will also be withdrawn from assets and are included in the Maximize Net Worth solve noted above.

Will her current asset base support this? It will, and below is the comparison where Strategy 1 is her current plan without the new life insurance, and Strategy 2 includes the IUL as described above. Due to the addition of the IUL (and its participating loans), the long-range gain in net worth of Strategy 2 vs. Strategy 1 is over $20 million, an astonishing increase. 21st century investment-grade life insurance is truly amazing, and it is the key component in helping Dr. Rand avoid a $20 million dollar mistake by acquiring the term insurance.

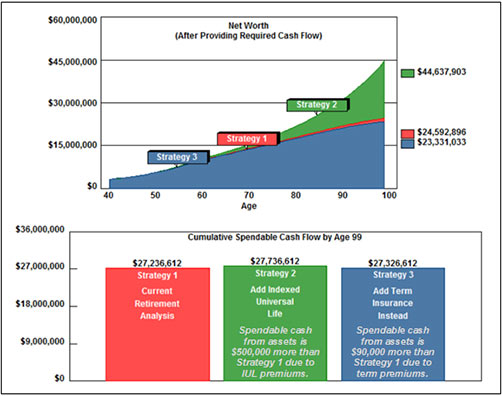

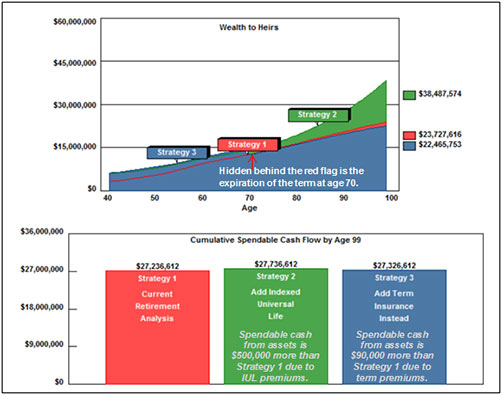

$3.6 million of 30-year, level term insurance costs $3,600. Let’s substitute that for the IUL policy and see what happens. As you can see below, Strategy 3 with term insurance is not suitable from the standpoint of long-range net worth and wealth to heirs.

The difference in wealth to heirs is over $16 million in favor of the IUL vs. term insurance.

Critical point: The gain in net worth and wealth to heirs is accomplished with no additional out-of-pocket costs to Dr. Rand as premiums are funded by withdrawal from her assets; however, it is only the IUL that produces serious increases in wealth due to its participating loans, cash value, and death benefit.

The Suze Ormans of the world tell Dr. Rand to buy the term insurance. They are wrong!

For licensing information regarding Wealthy and Wise, contact Julie Nayeri at julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President - Sales, at dag@insmark.com or 925-543-0513.

InsMark’s Digital Workbook Files

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

Digital Workbook Files For This Blog

Download all workbook files for all blogs

|

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark System. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

Note: Wealthy and Wise produces a significant number of reports since we never want you to have a client, attorney, or CPA ask, “Where did this number come from?” There is backup for every number, and in this Blog for example, there are four full evaluations: 1) Comparison of Alternatives; 2) Current Retirement Analysis; 3) Add Indexed Universal Life; and 4) Add Term Insurance Instead. Each one in the series produces different mathematics thus the large number of reports. You will likely want to pick and choose various combinations of reports to share with your clients, but you will always want to have access to all of those pertinent to your overall analysis.

Click here if you would like to review the 100+ page report for Dr. Rand generated by the System.

InsMark’s Referral Resources

(Put our Illustration Experts to Work for Your Practice)

We created Referral Resources to deliver a “do-it-for-me” illustration service in a way that makes sense for your practice. You can utilize your choice of insurance company, there is no commission split, and you don’t have to change any current relationships. They are very familiar with running InsMark software.

Please mention my name when you talk to a Referral Resource as they have promised to take special care of my readers. My only request is this: if a Referral Resource helps you get the sale, place at least that case through them; otherwise, you will be taking unfair advantage of their generous offer to InsMark licensees.

Save time and get results with any InsMark illustration. Contact:

- Ben Nevejans, President of LifePro Financial Services in San Diego, CA.

Testimonials:

"As I’ve said to anyone who will listen, Wealthy and Wise is the best piece of software in the industry."

Simon Singer, International Forum Member, InsMark Power Producer, Encino, CA

“Major cases we are developing have all moved along successfully because of the sublime simplicity and communication capability of Wealthy and Wise. I guarantee that the proper use of this tool will dramatically raise the professional and personal self-image of any associate who dares to take the time to understand it.”

Phillip Barnhill, CLU, InsMark Power Producer Minneapolis, MN

![]()

More Recent Articles:

Blog #37: Four Ways to Smite a Termite

Blog #36: The Magic of Indexed Universal Life

Blog #35: Revisiting the Pothole in Wealth Planning (Good Logic vs. Bad Logic™)

Blog #33: Referred Leads – How to Use Them Effectively

Blog #32: Documents On A Disk™ is Now in the Cloud

| 3 Reasons Why It’s Profitable For You To Share These |

| Blog Posts With Your Business Associates and |

| Professional Study Groups (i.e. “LinkedIn”) |

Robert B. Ritter, Jr. Blog Archive

Good concept but 2 weaknesses. $20 million is shown at age 100 well beyond her Life Expectancy. Also illustrating IUL at 7.5% is too high by any true professional’s view.

You are right, Stephen, Elizabeth Rand’s life expectancy is closer to 85 (preferred risk, non-smoker), but it also means that half of that age group is still alive at 85. So it did not seem unreasonable to carry the illustration to age 100 since some of her group will live that long and the reports and graphics could allow later evaluations. But even using age 85, it’s a $6 million net worth mistake not to acquire the life insurance; at age 90, it’s $9 million mistake; at age 95, it’s $14 million mistake.

I believe the interest assumption used on an IUL policy should reflect the client’s overall investment posture. In Dr. Rand’s case, all her equity-related assets are assumed to grow at 7.50% to 8.50%. (This is covered in the material you reference.) While I have no issue with an alternative evaluation using more conservative overall assumptions on all her investments (including the IUL) , I think it’s unrealistic to single out the IUL for inferior interest assumptions.

I hope, in general, that the Dr. Rand study was useful to you in terms of the logic of a comparative analysis using our Wealthy and Wise System proving that retirement plans are typically more favorable when cash value life insurance is included.

Thanks, Stephen, for commenting.

Bob Ritter

InsMark President

It was helpful but the Commission that is reviewing IUL does not think the interest assumption should be so high. I appreciate the comments beyond her LE. Love Wealthy and Wise!!

Steve, I hope that the Commission that is reviewing IUL deals more with suitability than with an order to use lower interest rate assumptions — maybe by way of a suitability requirement that helps the prospect self-identify his or her risk tolerance. Clearly, an aggressive investor will want to see IUL illustrations using more aggressive interest rate assumptions that are tied to indices he or she believe are valid selections, just as a conservative investor will want less aggressive interest rate assumptions. To that point, at the 2015 InsMark Symposium in late March, we are introducing a new module in the InsMark Illustration System that provides such a suitability questionnaire as well as a 4-way Comparison of Insurance Plans illustration comparing illustrations of Whole life, Universal life, Indexed Universal Life, and Variable Universal Life with the idea that the suitability questionnaire will guide the producer and the client into a making a responsible purchasing decision.

Unfortunately , the big mutuals are behind the push to limit the yields shown for IUL illustration because they have a serious difficulty in competing with IUL due indexed yields and participating loans. I’m reminded of an advertisement by MassMutual in the early 1980s with a line something like this: “When MassMutual Offers Universal Life, You’ll Know It’s OK to Buy It.” A few short years later, MassMutual offered universal life. One day, I suspect the mutuals will also offer IUL.

Thanks again for commenting, Steve. And thanks for the nice remark about Wealthy and Wise®.

Bob